AGL might have a new Chair and an activist shareholder but decarbonisation progress is slow

This note was originally motivated by Jeff Dimery, CEO of Alinta and, in my opinion, a highly competent CEO. Jeff observed on a social media platform that wholesale electricity prices were flat but retail tariffs had gone up considerably. Jeff mentioned “environmental taxes and network costs and bemoaned that there wasn’t more gas”. The note made me curious and so I already wrote a note about the retail tariff side of things, and now I want to get to the nearly trivial cost of environmental taxes in electricity bills paid by small consumers. And the hidden cost that is being paid by my grandkids and their children.

To be honest what got up my nose were Jeff’s social media comments was the remarks about “environmental taxes”. He didn’t say so but I assumed he doesn’t approve of environmental taxes. In my opinion emissions facilities should be taxed much more heavily to reflect the social cost of carbon (see figure at end of note). I find it astonishing that CEOs of major emitters still dont take emissions to heart. Not just seriously but to heart. It’s a privilege to be CEO, a very highly paid job, and the decisions that CEO’s of big business make influence many things directly and indirectly. Science and the observable reality is that climate change is a big deal. CEOs are the ones to lead the charge. Along with the rest of the Board. If that makes me woke and a greenie well as Bob Dylan said, “they hype you and type you, 20 years of schooling and they put you on the dayshift”

What are these environment taxes? Mostly they are REC prices right now, but also I guess you could include out of the money CFDs for renewable energy, and there are probably NGACs and VECs and other things even I can’t be bothered with.

REC prices have in fact declined in the past year, quite sharply and conceptually are due to expire in 2030. It’s well established that the reason REC prices held up was because of voluntary surrender. That organisations, often but not always. Govts throw their RECs in the bin. Last time I heard an estimate something like 30% of RECs were thrown away. Organisations that need RECs, primarily retailers therefore had to pay more to get what was left.

As measured by the AER for the purposes of the DMO and for the record the environmental cost paid by consumers has hardly changed in $/MWh in the past five years. (Its been about $21/MWh out of a total cost in 2025 to an Ausgrid consumer of $465/MWh)

Reviewing the CO2 data of the top emitters

In late February each year, at least under the current Federal Govt., the DCCEEW releases an annual update of the top emitting facilities and the ownership of those. Given Jeff’s comments, and given the imporatance of emissions to the future generations it seemed appropriate to review the data.

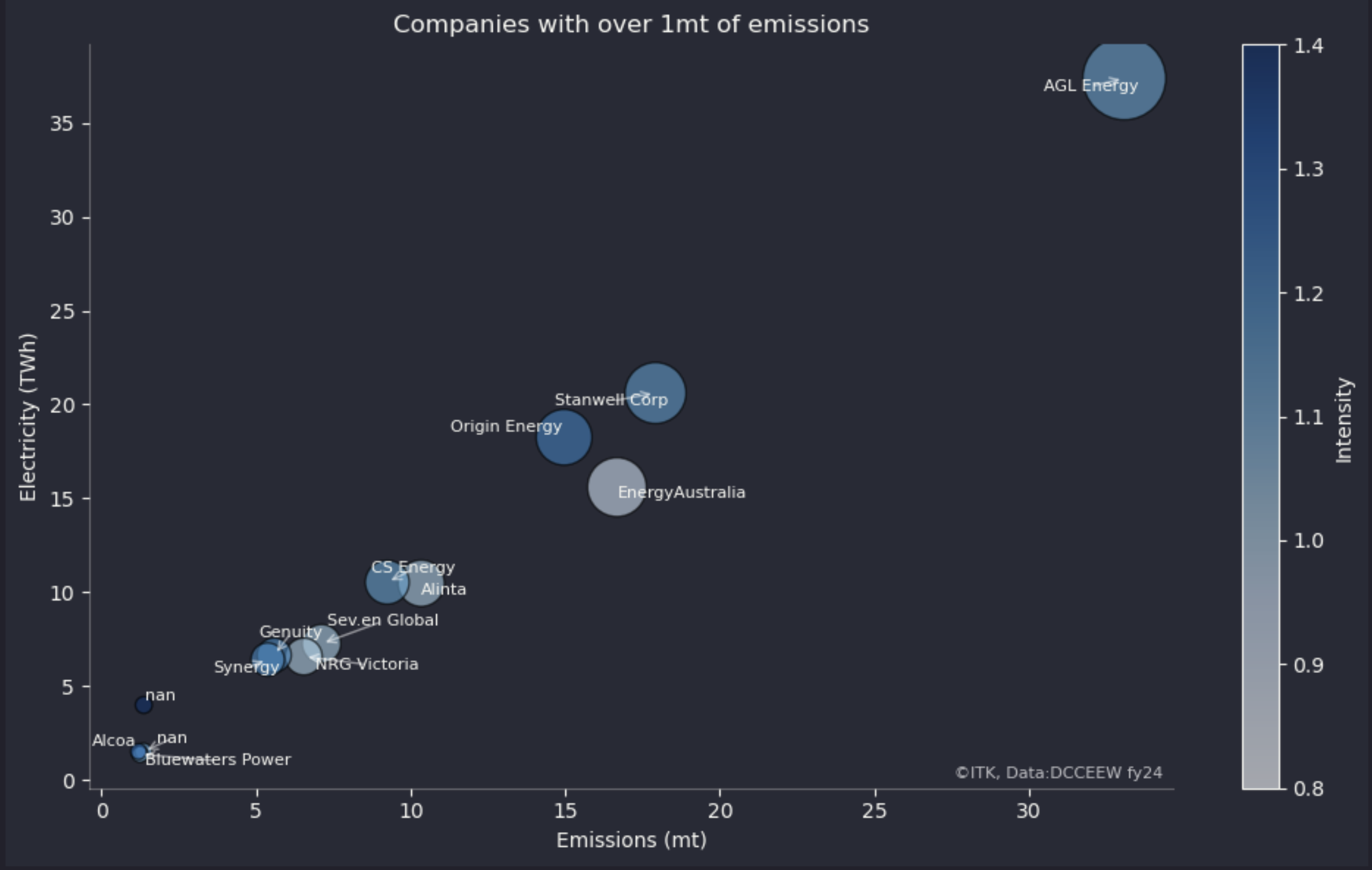

There are a couple of overarching comments. First it’s a good thing in my opinion, that around 30% of total emissions are owned by a few companies.

Second AGL’s closure of Liddell has made a difference to AGL although they are still way out in front.

First lets look by Company

AGL still stands in a league of its own, Stanwell is next but in 5th place is dear old Jeff Dimery’s Alinta. Alinta’s generator LYB has an emission intensity of 1.3 tCO2/MWh amongst the worst in the world never mind Australia. Fortunately, in my opinion, because it gets its brown mud (described as coal) from LYA’s mines its unlikely to be viable once LYA closes.

And when you look at the chart it is a reminder that AGL is responsible for something like 5% of total emissions in Australia from all sources. This is a company which has a shareholder Grok supposedly committed to decarbonisation, it has a new Chair Miles George who was previously CEO for many years of Infigen, a wind developer and committed to reducing emissions. Yet what has AGL done? Its announced that like every big Gentailer its going to build some batteries and maybe buy some output from Tilt or Pottinger in due course. But not this year.

The second biggest emitter is the QLD Govt owned Stanwell. Stanwell had strong plans to reduced its average intensity by causing wind and solar to be developed. In this regard it is far ahead of its sister company CS Energy. it remains to be seen what the change the new QLD state Govt, owner of Stanwell does. As we know the QLD Govt called in for a 30 day review 4 large wind farm projects. That 30 days must be rapidly expiring.

Behind Stanwell comes Energy Australia where to its credit intensity will soon be reduced by the closure of Yallourn, and then Origin which to its credit is soon to close Eraring. For both generators the closures are partly driven by economics but at least in the case of Origin there does seem to be some concept of the need to decarbonise. My sense is that ORG is getting ahead of AGL and EA in facilitating new VRE supply. Its projects in New England and of course Yanco Delta are substantial. By contrast Tilt and AGL sit around with Liverpool Range seemingly waiting for Godot.

Having the emissions held by a only a few owners makes it easier to manage

The entities in Figure 1, the top 15 emitters in Australia, are responsible for 132 mt of CO2 equivalent which is about 29% of Australia’s total 460 mt of emissions. And at least 2 of those big emission generation plants Yallourn and Eraring should be closed within 3 years. However its disappointing to report that despite the closure of Liddell total emissions from the top 15 emitters declined only 1 mt or less than 1%.

The QLD Govt if it was minded, that is if actually cared about the future of Queenslanders would continue with the well defined program of closing QLD’s coal generation units over the next 10 years. The disappointment of the former QLD Govt was wasting the first 8 years of a 12 year term.

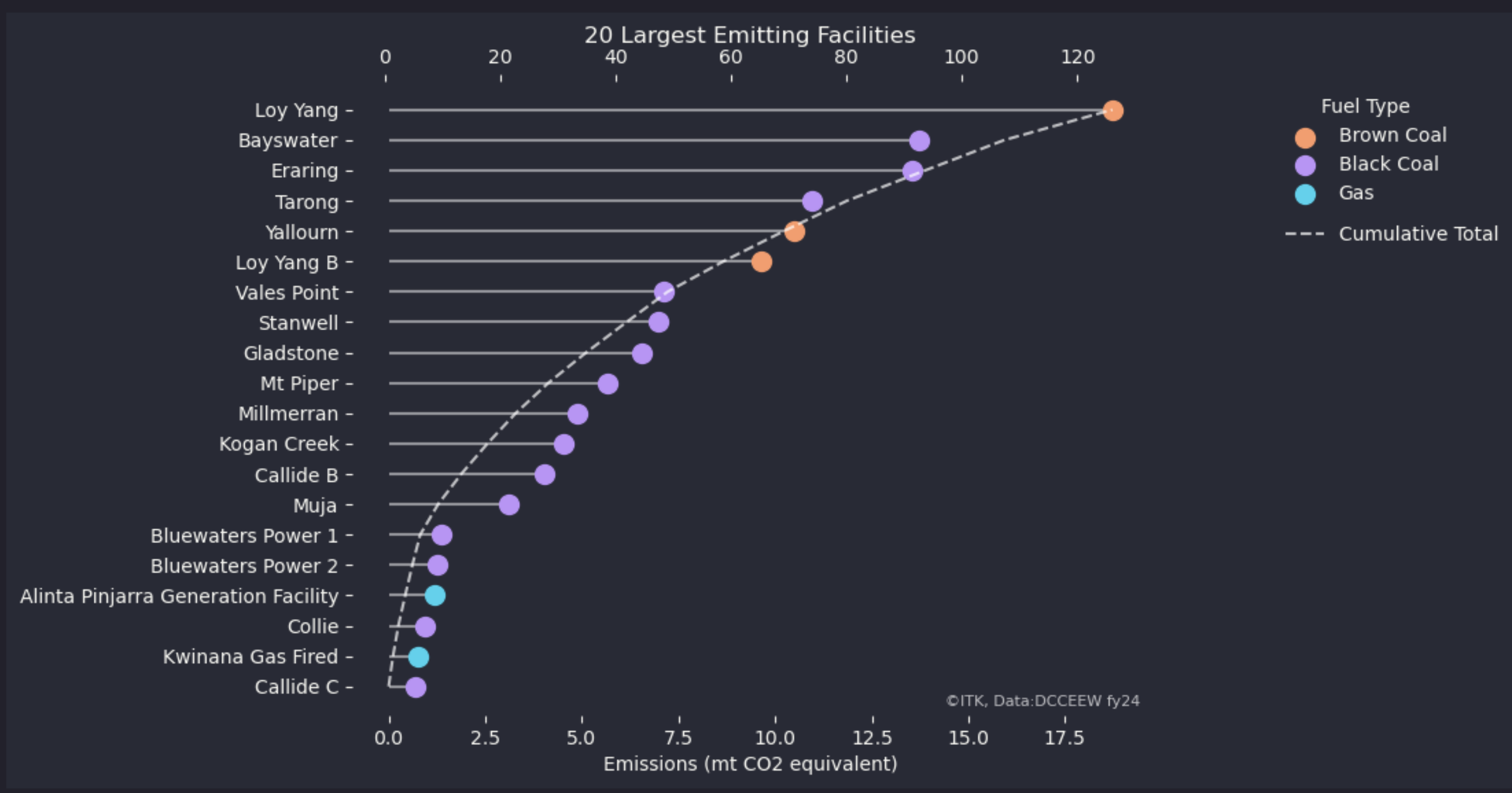

A reminder of the big emitting facilities

Just a reminder of where the emissions come from.

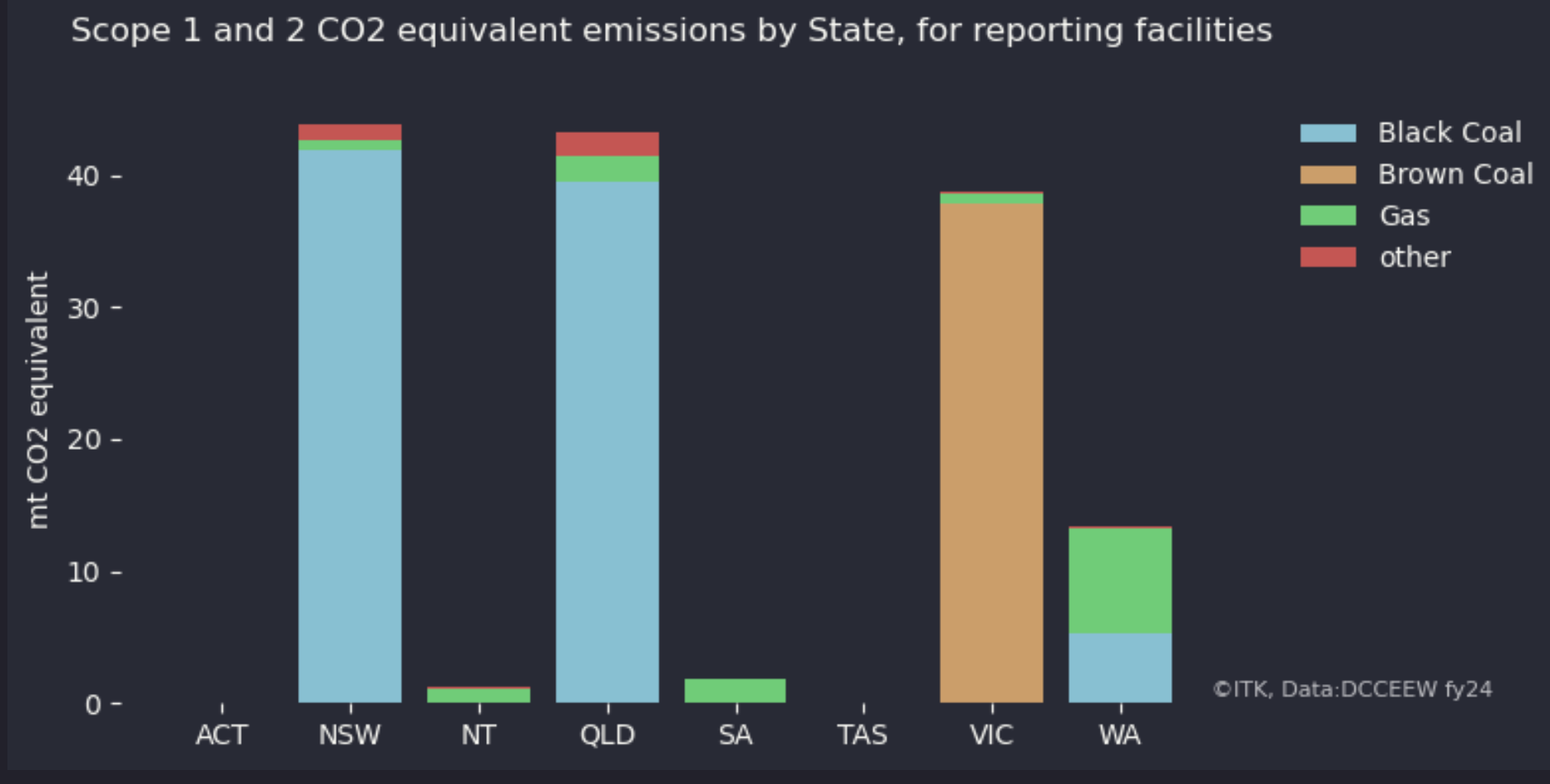

And by State

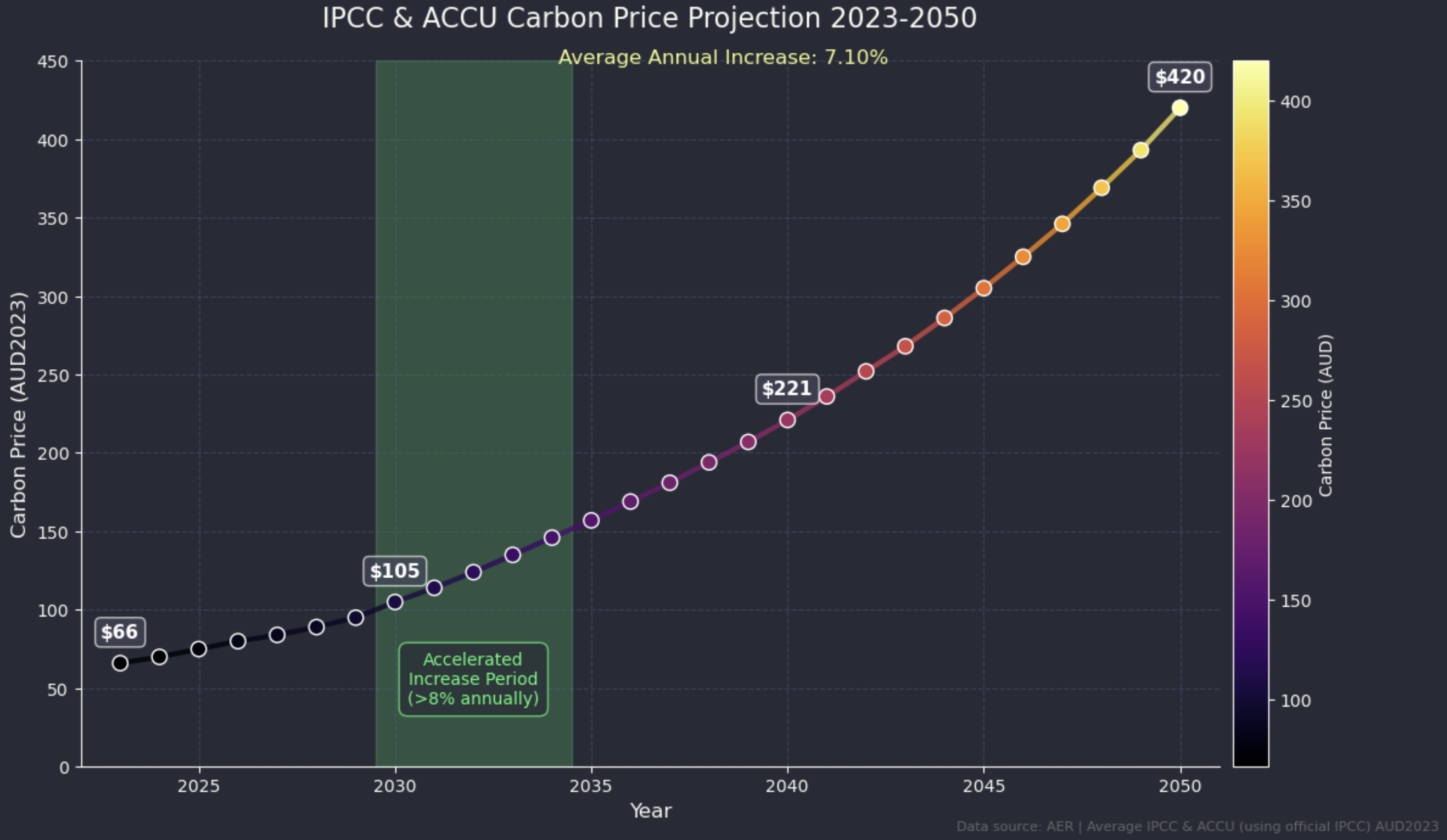

AER’s present estimate of Social Cost of Carbon

This is the tax that none of these emitter actually pay, but should be paying.