Going off the reservation

In summary a brief headline review of the gas situation is.

There is a limited amount of for sale uncontracted gas, perhaps 100 PJ a year but likely less where the Federal Goverment could force down the price. That gas has to be offered to the domestic market first but at the current price, around $14/GJ demand is limited and some of that uncontracted gas is sold into the spot LNG market. Forecasts for LNG prices vary, but arguably US shale based LNG is currently seeing some cost pressure.

Forcing the price down for that gas might lead to more gas generation but is unlikely to have much impact on peak electricity prices because peak electricity prices aren’t set on the basis of marginal cost but rather on the basis of what the market will bear. Batteries charge higher or similar prices than gas but have far lower fuel cost. Hydro has no fuel cost but charges what the market will bear. Gas is the same. Gas won’t price below cost but it sells well above. I hope the LNP understands that but given their form to date it seems unlikely

Rather than a lower price, to make peak electricity prices go down via gas requires:

- a larger quantity of gas;

- more gas generators and;

- more diversity of ownership of gas generators.

I find it difficult see independents getting into gas generation and competing. It’s very very far from my world view for a whole variety of good reasons. Gas is expensive, gas generators are hard to build and expensive, pipeline rental costs are high and best spread over a bigger load and gas generators are not that good at managing the variability of wind, solar is a bit more predictable. Possibly more important there is plenty of evidence from the Texas and Californian markets as well as Australia that market participants are far readier to invest in batteries than gas generation. It’s not even a competition any more. It’s a done deal.

While we are on a competitive market trip let’s not forget that the upstream part of the market is far less competitive than even the generation and retail market. In the upstream Eastern Australian market when you talk about new developments you sit across the table from a close to monopolistic supplier Santos. The LNG players only interest in Australia is volumes they have to sell in this market. LNG producers want to export. It’s entirely speculative in my amateur hour musings but I’d not be at all surprised if the LNP hadn’t asked for Santos’s opinion about any proposed reservation scheme.

Forcing the price of gas down might slow down the existing demand destruction in industrial, commercial and residential sectors but only a bit. Electrification of heat, and consumer preferences are shifting demand away from gas anyway.

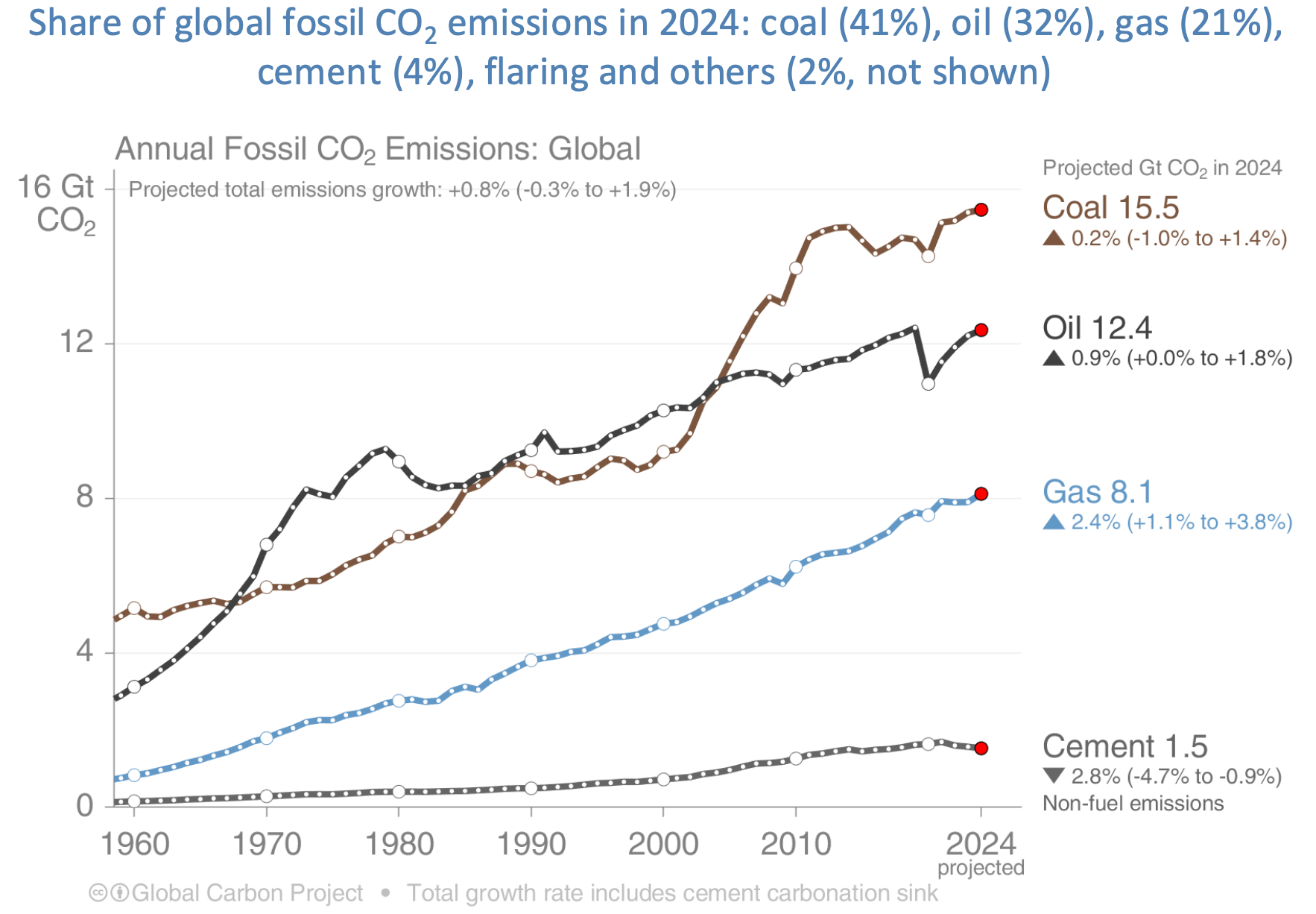

Although the LNP has no interest in the following. Gas is 20% of global annual emissions and the 2.4% compound annual growth rate in emission from 1990 to 2024 is faster than either coal (2%) or oil (<1%). If you are a gas apologist you would say that gas emits less carbon than coal so replacing coal with gas is a decarbonisation strategy. It is not. Slower CO2 growth is not the same as decarbonisation. Spending all those $billions on replacing coal with Gas as the USA has done is hardly better than China spending the same money on Coal. China has built the renewables to fix the problem. The USA contributes little or nothing. It freeloads on the efforts of the world in contrast to Europe which does all the hard work. What the USA has spent on defence Europe gives back in emissions reductions.

I’d spend money on getting a better view of the LCOE of the various upstream development options rather than on gas reservations

Looking further out you have to be quite the believer in the economics of 2C (that is quite speculative value) QLD CSG, and to believe that Narrabri CSG can be developed at a reasonable price to see any growth in gas or to think that Beetaloo is an “elephant”. Reminds me of the dad joke about the difference between a beetle, an elephant and a bucket of water, but no time. Bass Strait, Cooper Basin, and Otway gas reserves are all in structural decline. Cooper declines quite slowly as most of annual production is being replaced. In the Santos world new fields continuously replace declines in existing fields.

If prices are high enough then things can be done to reduce decline or even grow production but you can’t have low prices and more investment. In my view there are both more and less reserves than companies report. That is companies under report what they really have and over estimate what they think they have.

Personally I am happy that gas prices are high and gas is tight, but if I was advising the Goverment about good gas policy I would advise hiring some good people, and getting very good advice about 2C gas resources in QLD and the likely economics and prices of developing that gas. As things stand the 2C resource is not even that big relative to the 3P (proved, probable and possible) reserves on which contracts are based, let alone of a status to provide policy confidence.

There might be a lot of gas in the Beetaloo basin in Northern Territory but I doubt it will be easy to develop.

There is 2000 PJ of gas to be developed near Narrabri but Santos acquired Eastern Star in 2011 and there are still ongoing court cases and the FID not made. But it probably will be. That gas is likely to be a lot more expensive that Santos would have allowed for 14 years ago. Production could run to 100 PJ a year I guess. Narrabri didn’t rate a mention in Santos’s investor day, likely because of the legal sensitivity. Public information on the recent economics is very limited, although in February the capital cost was stated at A$3.5 bn by the Santos CEO according a newspaper headline in a paper I no longer subscribe to.

You could build 3 GW of combined cycle gas generation running at 40% capacity factor given 2000 PJ of gas but I wouldn’t want to own it and it likely wouldn’t be running before 2030 at the very earliest. Combined cycle economics are poor in a region with lots of wind because you are often operating at part efficiency. Alternatively you could build 1000s of MWs of open cycle peakers but these require capacity contracts and or high spot prices to be economic as capacity factors are low. Kurri Kurri ended up costing around A$2m/MW excluding gas connection, Tallawarra B as was A$1 million/MW as an add-on to Tallawarra A. This data makes me think Gencost’s estimates of $1-$1.3m/MW would likely be well on the low side.

The most likely new entrant as opposed to a new plant might be Squadron or potentially CS energy 400 MW at Brigalow. Existing generators with development plans include EnergyAustralia/Delta who have an approved 700 MW development at Marulan, AGL 250 MW approved at Port Stephens. (Project data source:WWW.Renewmap.com.au) You can’t rule this stuff out but I have my doubts.

Also and although I dont think it has many customers Squadron Energy’s LNG import terminal at Pt Kembla is likely in commissioning stage and ready to go next year. If it was attractive to build gas generation using LNG imported gas Squadron would already have built such a generator.

Governments can’t control price and quantity.

To be clear, in my world no new gas reserves would be developed and the capital would be put into electrifying existing demand for gas, mainly via renewable energy and process heat decarbonisation

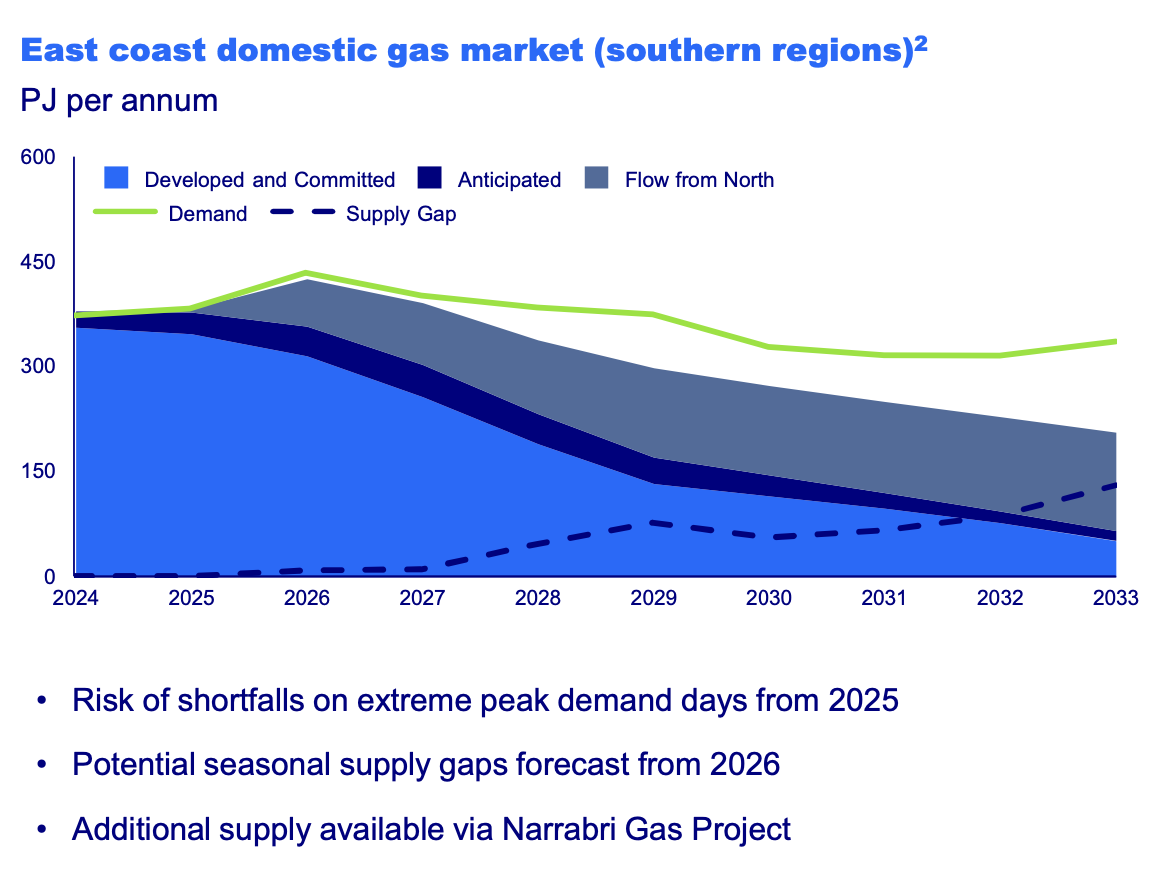

But if it’s amateur hour at the rodeo social evening then it’s generally agreed that Eastern Australia needs more gas to be developed for a constant demand. You could pick a version of this chart from AEMO or various other consultants and a chart from 15 years ago would have looked much the same.

On the other hands developers (actually the developer Santos) facing long and increasing delays to projects and high costs of capital, wants a decent return and that requires I suspect prices North of $10/GJ.

Governments seek to control price for their voters, the domestic market. Personally I don’t think most voters care about the gas price, except maybe in Victoria but business certainly does. In the end one of the oldest rules in markets is you can control price or supply but not both.

Uncontracted gas is a volatile balancing item in total demand

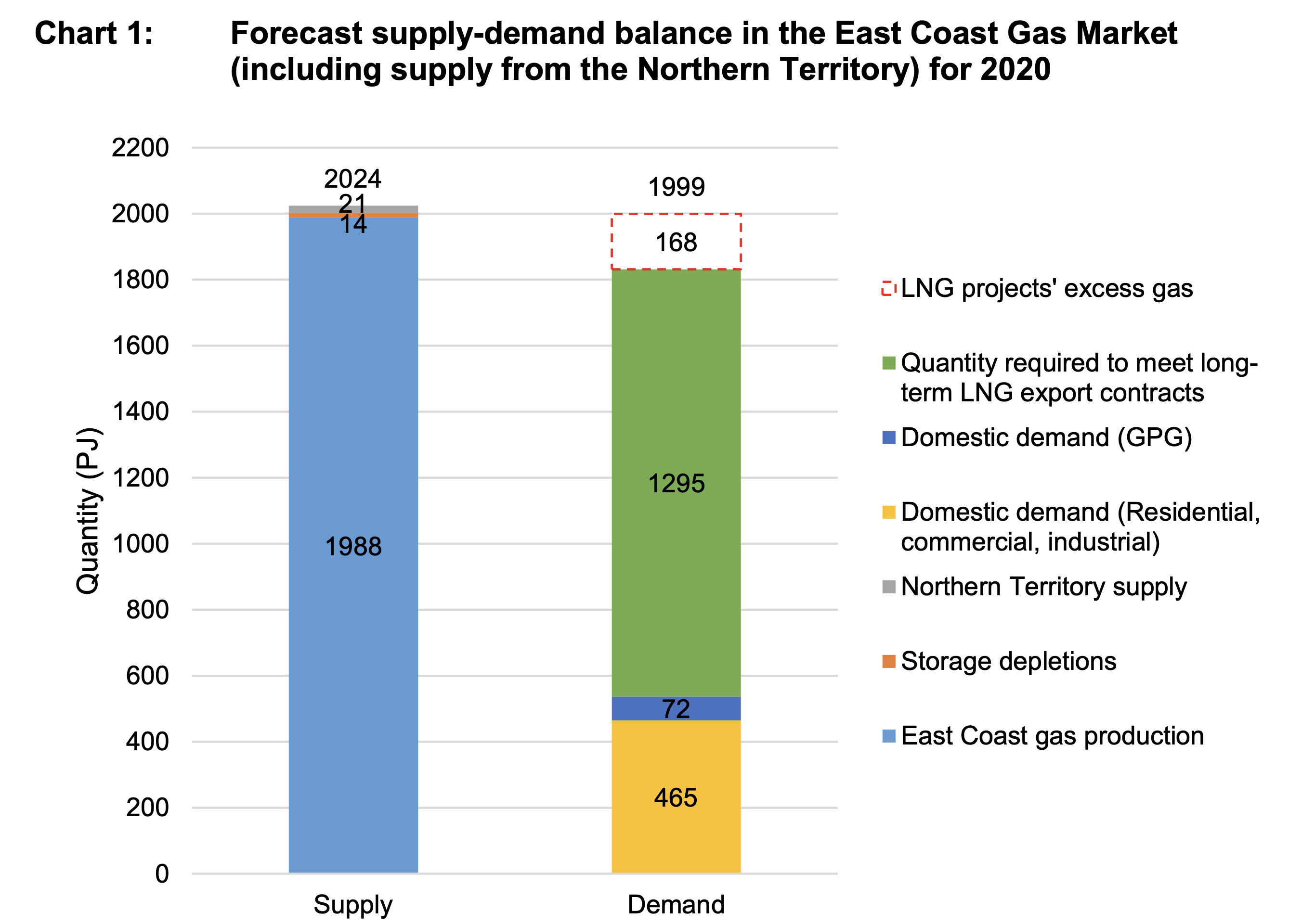

Thanks to the ACCC there far better information on gas supply and demand is available to day than ten years ago. In particular the ACCC estimates and regularly updates the amount of uncontracted gas available either for export or for sale to the domestic market.

In 2019 when preparing forecasts for 2020 the ACCC found that there was as much as 168 PJ of gas supply over what was required and contracted.

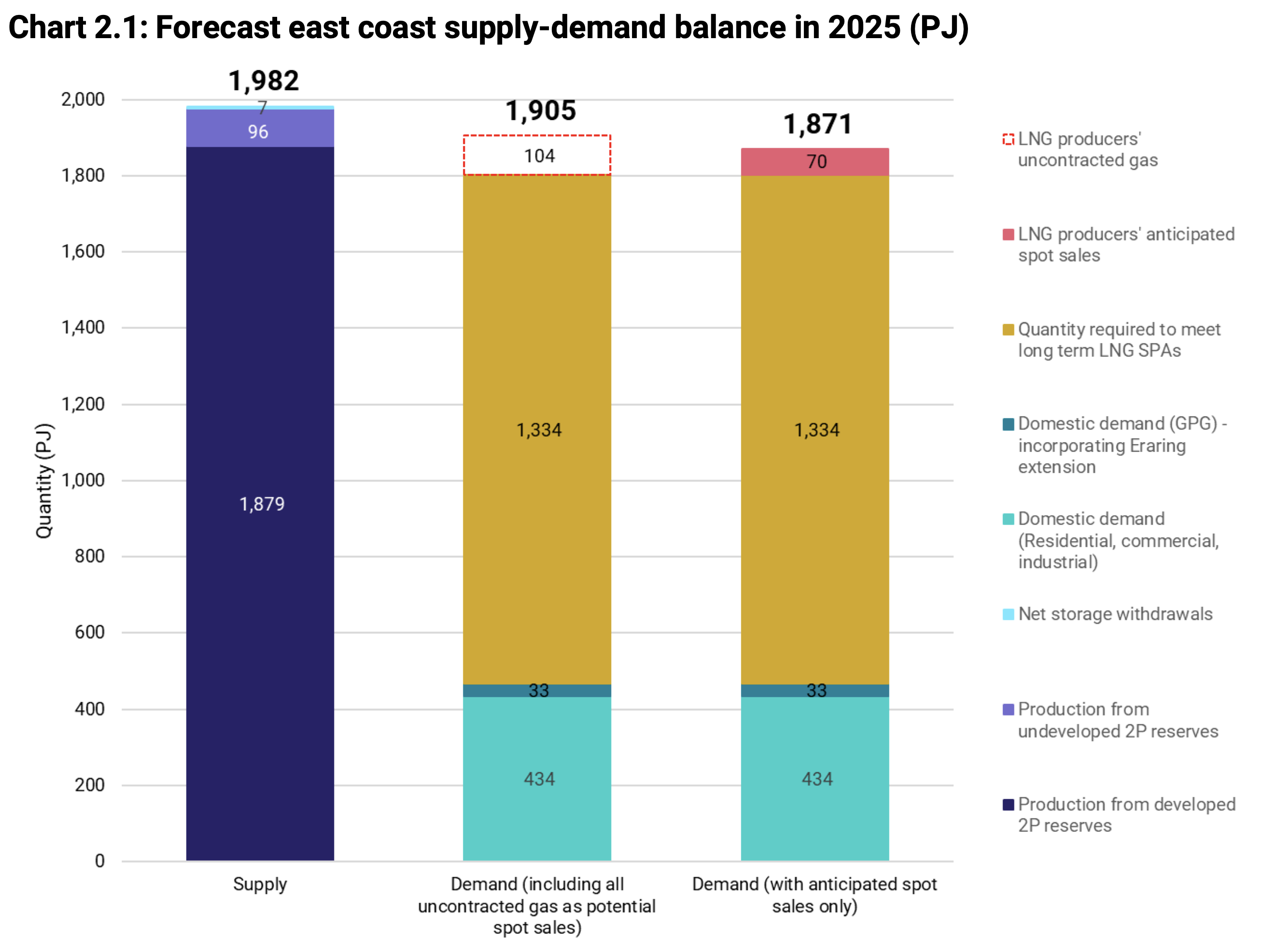

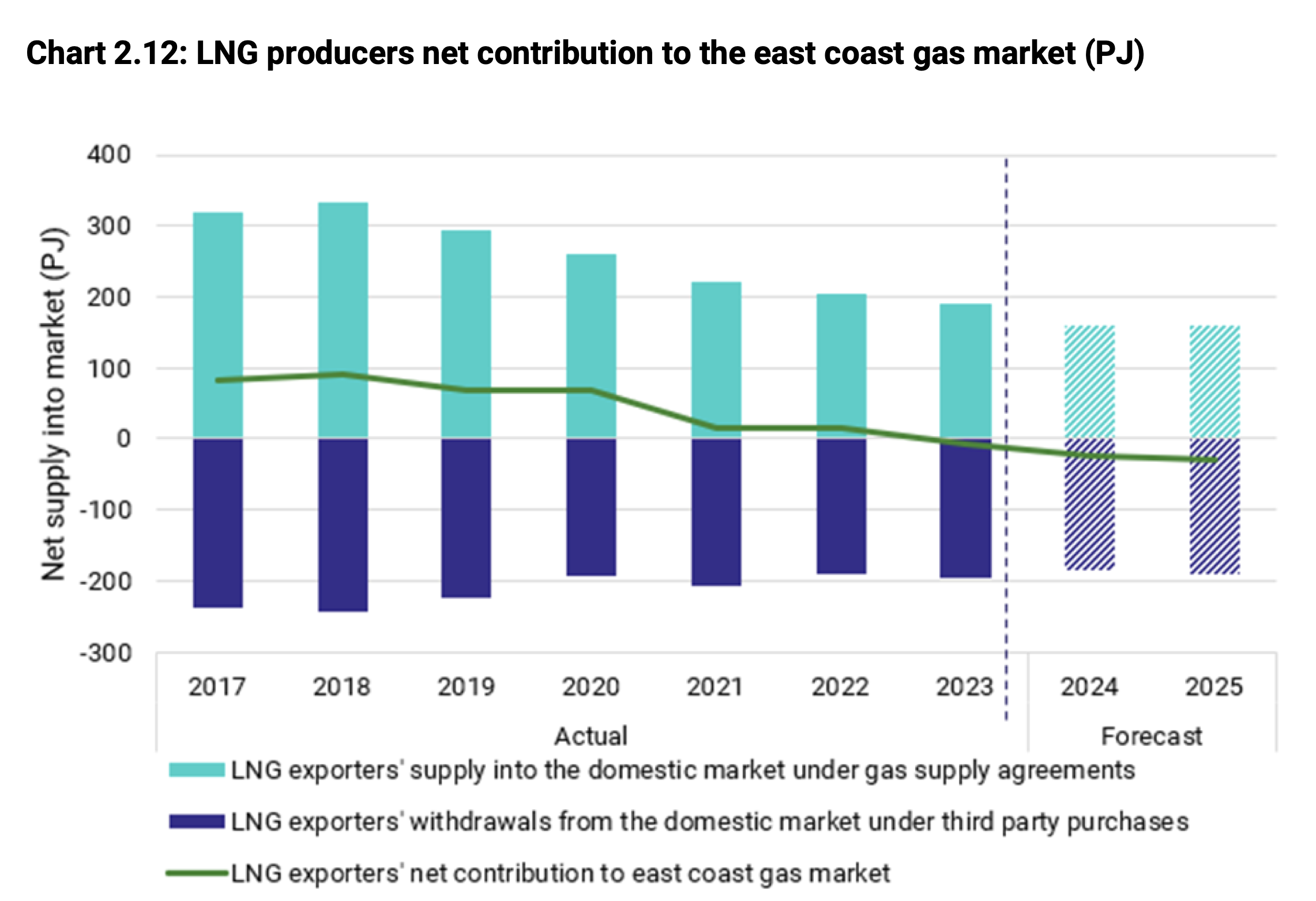

Fast forward to 2025 and the net uncontracted surplus has declined and that’s despite a decline in domestic non electricity related demand.

Before anyone points it out, I can see that the discrepancy between supply and demand forecast for 2025 as presented by the ACCC is unacceptably large and I could not easily find the explanation. But I have taken the figures as presented after eliminating Northern Territory production from the earlier numbers.

Also we need to think about both quantity and price. Some, indeed most of the uncontracted surplus is sold on the domestic market. Nevertheless the net supply from LNG exporters to the domestic market which was close to 100 PJ in 2018 now appears to be in net deficit. Put another way The LNG producers increasingly need to buy gas from the domestic market to meet their export contracts.

and based on ITK’s weekly update of the STTM market (NSW, SA & QLD) prices are around $14/GJ. One might argue that the gradual tightening has driven price right up to export parity.

Daves explanation of why prices went from $4.50 to $9 and now $14/gj

The simplest explanation of why gas prices went up over the past 15 years is that Santos wanted and caused them to go up. From about 2005 onwards the Australian gas producers could see that prices in Eastern Australia were low by global standards, but there wasn’t enough gas supply or demand to change anything. When it became clear that coal seam gas (CSG ) in QLD was of sufficient quantity and price to build an LNG industry the opportunity to link international prices to domestic prices arose.

Origin, now APLNG, and QCG (now Shell) had enough gas to build two LNG trains each, but despite being the largest producer in the Cooper Basin, Santos did not. At the time Santos was too slow in buying reserves in Qld and, in my amateur opinion, the reserves it did have were not of the same uniform quality. Nevertheless Santos was able to talk its consortium partners into building two LNG trains even though there was only enough gas for 1.5 trains.

That continues to this day. For instance STO 2024 investor day states:

“GLNG 2024 expected gas supply mix:

• 62 per cent GLNG upstream equity gas

• 15 per cent other Santos equity gas

(including Cooper Basin)

• 23 per cent other third-party gas supply”

This created a constant demand for gas to export and various contracts were signed not just by GLNG but also by Shell buying up all or most spare gas and devoting it to the GLNG and QCLNG.

This occurred at the same time as Bass Strait reserves were diminishing and Otway Basin supply was always of very short duration. Promised unconventional gas from the Cooper Basin hasn’t really turned out that well, although it is trickling out.

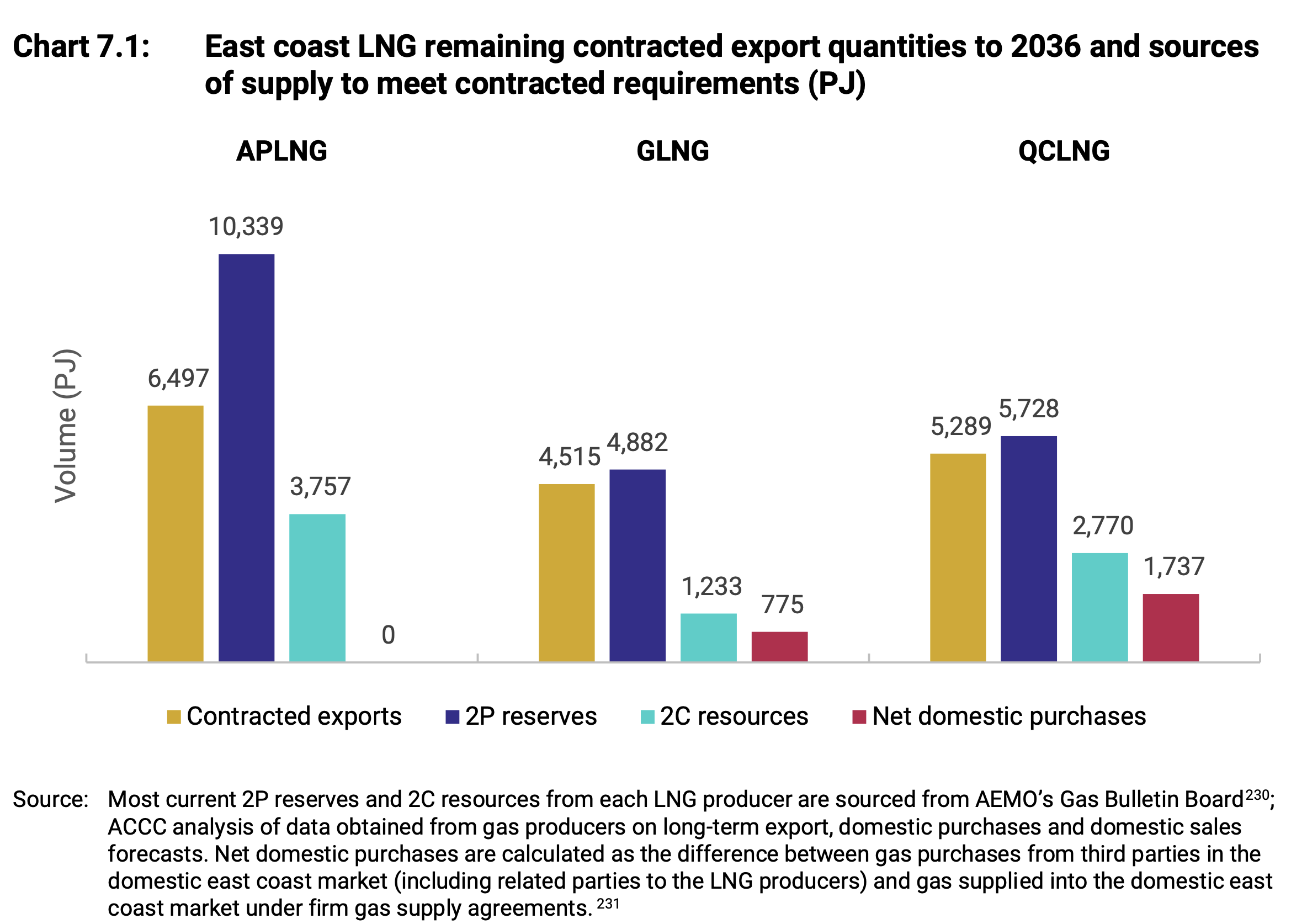

The contracted situation of the QLD LNG producers was shown in the following figure from the Dec 2024 ACCC report.

I can agree that in this figure QCLNG looks to have done more to tighten the market than GLNG. However that’s really QCLNG (Shell) purchasing from Shell/PetroChina . The ACCC noted that the foundation contracts of the Qld LNG producers expire around 2036 and that is when the real opportunity for a meaningful reservation policy arises. I’d want some convincing that gas production from Arrow’s SGP North project was going to be particularly profitable. Its the next new field being developed with production of around 40 PJ per year targetted.

Equally taken at face value the only business that has enough 2P (proved + possible) reserves to be impacted by a post 2036 domestic reservation policy is APLNG.

In conventional gas 2C that is “contingent” resources sometimes turn into reserves but they aren’t really bankable. My concern is that as reserves get run down the possibility of rising costs and negative reserve calculations can happen. Equally technology, in this case gas substitution, can impact reserve economics.

And of course by 2036 I am pretty confident that electrification will be a lot further down the track and that the use of gas for electricity production will end up being less than AEMO forecasts not more.

Santos is the only gas company of any substance really interested in Eastern Australia

BHP/Esso have long since stopped thinking about investing in Eastern Australian gas, Beach is a bit part player, Origin has steadily reduced its upstream gas interests. There are a bunch of minor players but without having done the formal counting my feeling is that Santos owns the non LNG reserves and if you want to get more gas in Eastern Australia whether it be from CSG in Narrabri, unconventional gas in the Cooper Basin or “elephant resources” at Beetaloo in the Northern Territory its Santos who will be sitting across the table.

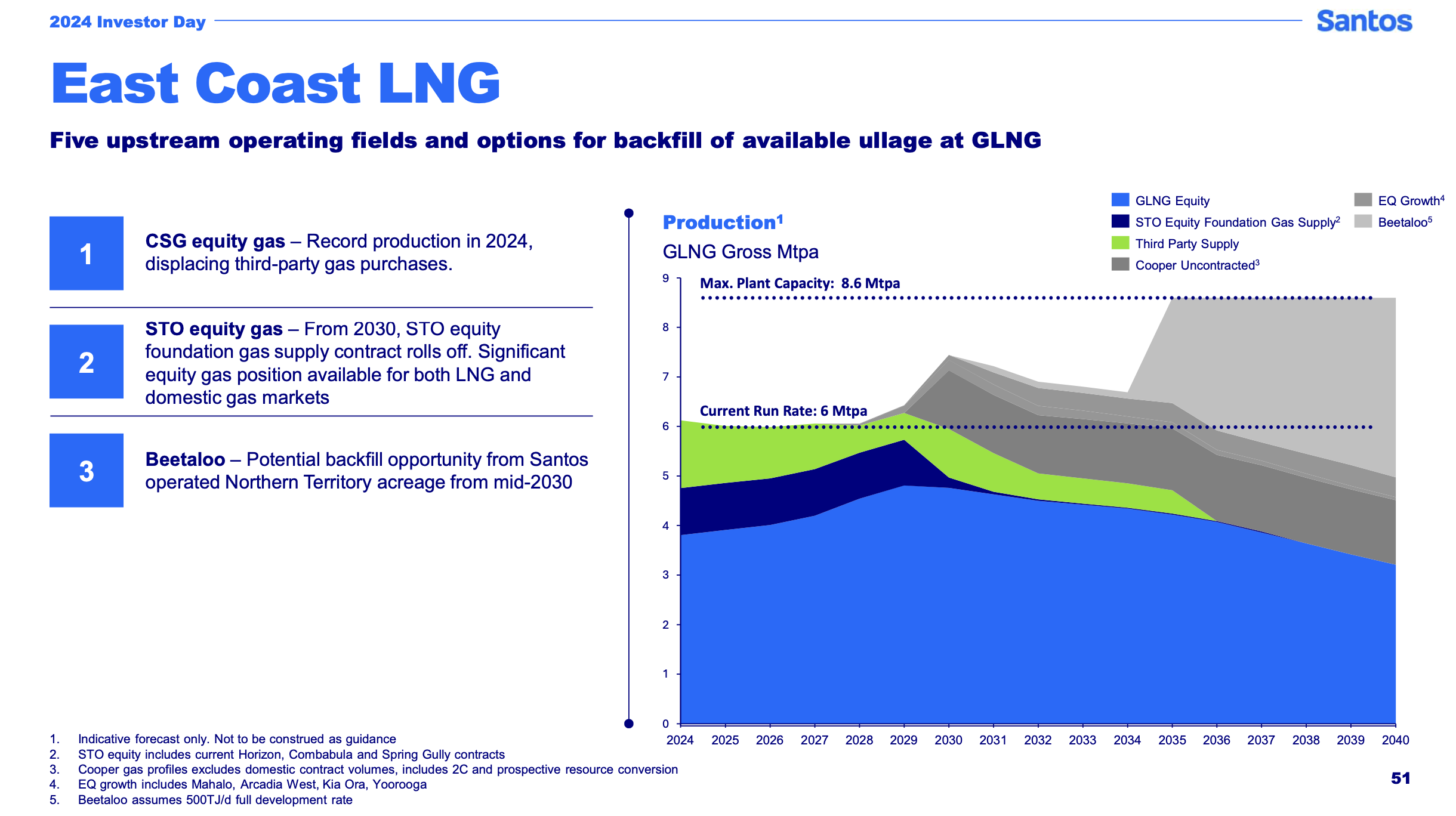

You can get the idea by looking at what Santos projects just for GLNG.

In this world there is always another project. For those counting Beetaloo 500 TJ/day is about 150 PJ per year and would imply about 4,000 PJ to GLNG and no doubt some going off to Darwin as well.

There is also the implication in STO’s point 2 that once STO’s existing equity gas contract sales to GLNG roll off starting in 2030 remaining reserves will be sold to the highest bidder and STO assumes the price will be a lot higher. Of course that is before a reservation scheme.

Gas demand is declining, due to price driven demand destruction and electrification

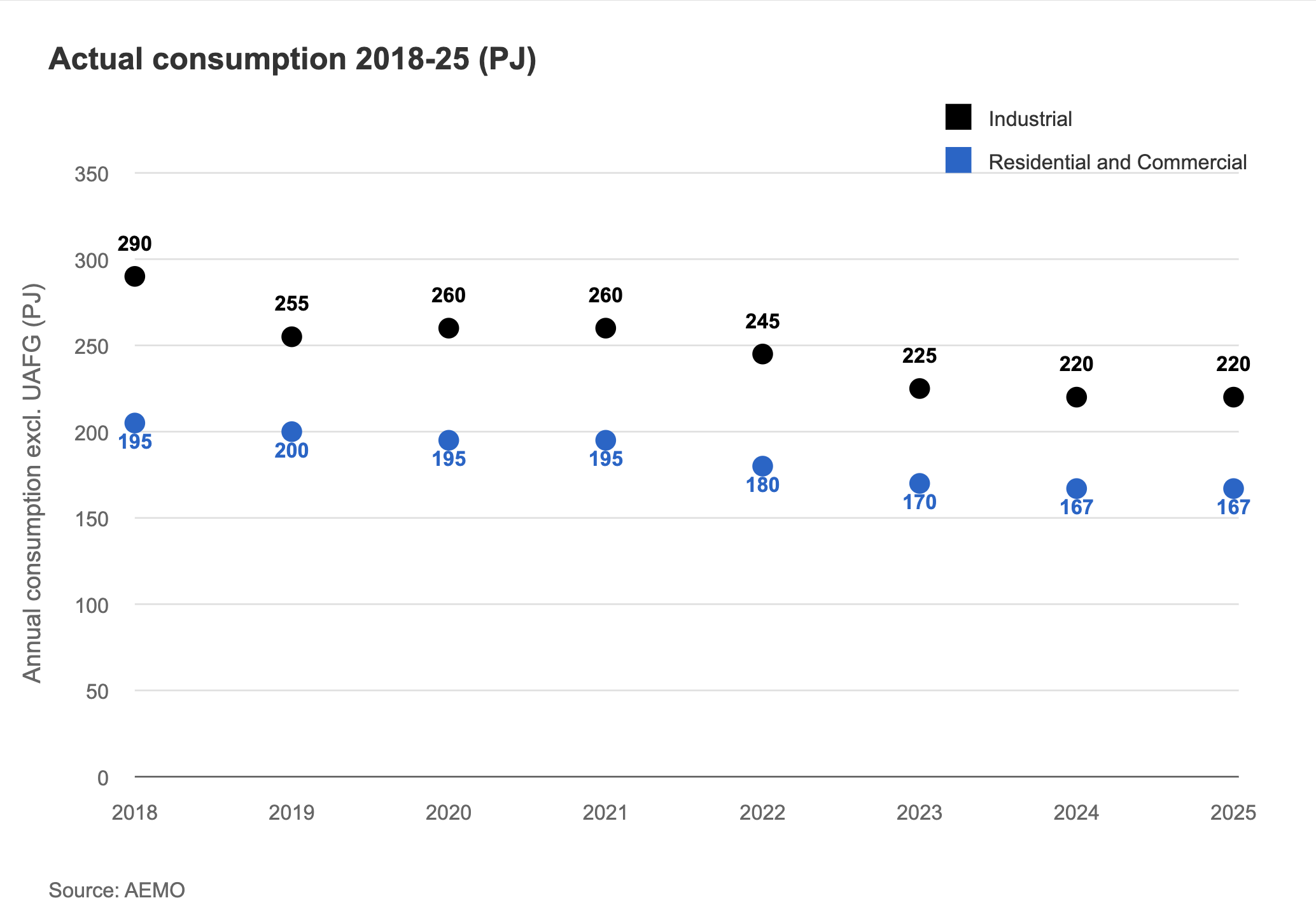

High prices incentivise business to reduce gas use mainly via substitution. For example Incitec closed down a fertiliser factory in QLD due to high prices in 2022 freeing up 14 PJ of gas supply. Another indication of market tightness is that contract tenor has shortened. The following figure does not include West Australia nor LNG its conventional consumption in Eastern and South Eastern Australia

Further declines are likely as the lagged impact of higher prices drives investment. Much of this would likely happen just due to price but there are also electrification efforts underway, but this is too big a topic for this note.

Gas charges way above cost. Cost is NOT the driver of gas generation price

Whether the LNP makes the cost of gas for electricity $14/GJ or $2/GJ doesn’t actually matter that much. What matters is the extent of competition to set the electricity price amongst gas generators or other suppliers to the peak price market. And since Snowy, Origin, and in some areas AGL and Energy Australia control the gas generation market you just aren’t going to see that much competition.

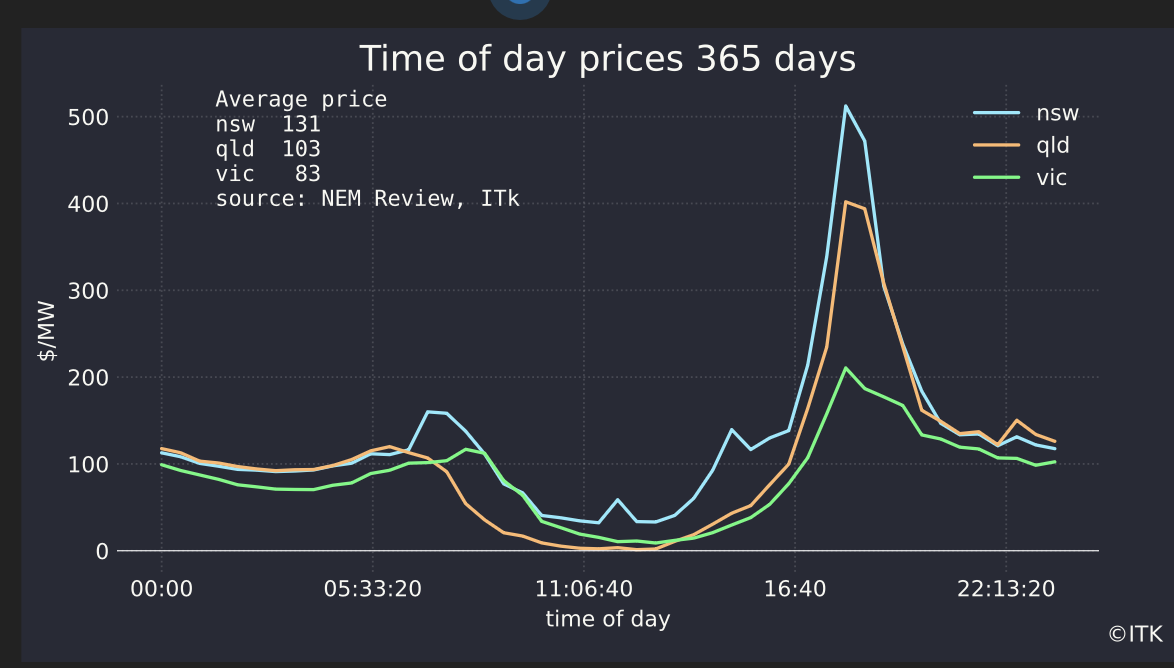

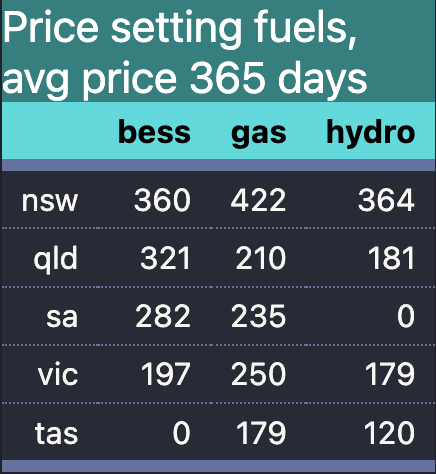

The following figure shows the average price of electricity over the day in the three main States. The price in the evening peak gets up to $500/MWh in NSW and $400/MWh in QLD and nearly $200/MWh in Victoria. In each case that peak price and the prices for the surrounding couple of hours are way above the cost of gas generation. Yes gas and hydro are setting the price but it’s got only a very little to do with cost. It’s about the fact there isn’t any competition at that time and they charge what the market will bear. Equally coal generators who have been running at a loss all day are more than happy when demand perks up to let gas and hydro set the pace. Coal follows along behind surviving for another season. And to be fair to the gas generators their capacity factor is generally quite low, so they have to make their money either from setting very high prices when they are running or more traditionally by selling insurance (cap) products.

You can see that that the price for each of gas, hydro and batteries is way above variable cost of production for each of the peak price setting fuels in every State.

And the inconvenient fact that of course there are the carbon emissions.

Of course Australia’s role as one of the world’s largest gas exporters surely has to mean something to Australians even if gas executives and shareholders cant give up the juice. I sometimes wonder how senior management at gas companies rationalise what they do to the lives of their kids and grandkids never mind everyone else’s but i guess it was ever thus. It’s the job of management to maximise NPV for shareholders subject to the law, not to worry about greenies.