Job done except…..

Electricity prices have fallen but….

If I just looked at what’s happened this year in the NEM I’d be feeling good. Remember the basic plan to decarbonise Australia and to provide a solid foundation for our continued health and prosperity is to:

- Decarbonise electricity;

- Electrify everything else thus decarbonising the economy.

It’s a very simple plan and for the most part very, very achievable. The underlying driver — although like Voldemort the name cannot be spoken — is to decarbonise and thereby reduce the already crippling and bound to increase costs of climate change. Whether that’s flood damage, drought damage, fire damage, health costs or damage to the barrier reef and its tourism the costs of climate change are high and increasing.

Although there are no doubt, no doubt multiple causes the fact staring every Australian household in the eye is that insurance is the fastest growing cost in the CPI.

More to the point business and Australia need a clear view of energy supply in three, five and ten years time. China sets a good example in this regard.

For want of a nail. No new wind so the machine will grind to a halt.

ITK owns a spot price forecasting tool. Not a trading tool but one that looks at how prices will evolve as the renewable share increases. It’s a very complete model, prices for every half hour to 2050 are solved via a linear program. The work we did over the past two years has emphasised to me how hard it is to forecast prices. The biggest issue is forecasting what capacity will be built and when, looking at LRMC and achievable build rates.

But all the forecasts I’ve done assume that lots more wind will be built. Because all the simulations show that building wind results in lower consumer costs than a system dominated by solar and batteries.

And the problem is that the wind isn’t being built. We all know it takes at least 3 years from the time of FID (final investment decision) to commission a large (400MW-1000MW) wind farm. In fact every such wind farm so far built is built in stages anyway.

None of us even talk about the CIS anymore. It pains me to say this, but so far it has utterly failed in its main job which was to induce new supply. I personally have long thought that just negotiating a 20 year PPA was all that was really required. I still think that’s the case. It worked in the ACT, it worked in Victoria, it worked via the State Owned generators in QLD. It would work in NSW.

Eraring can’t close, let alone Bayswater, Mt Piper or Vales Point unless there is overnight energy. That energy can come from either batteries or wind, or you can invoke pumped hydro or gas. Gas is totally unrealistic. The idea that enough pumped hydro could be built in the next four years can be laughed out of the board room.

The wind projects exist. The CIS awards exist. The transmission exists and will now be completed in both Orana and the South West before the wind farms. The social license in both regions exists. But the developers have fallen behind. Despite years and years and years of development they can’t get their projects over the line. At a minimum these projects will be late.

As I say without the wind the coal generators can’t easily close. You can make a case there is enough supply to close Eraring but it’s not a great case. Eraring’s economics are going to suffer as batteries eat into evening price, but from NSW Government’s point of view the supply risk is the main thing. There is also an argument about frequency control, but for me that is a bit of a furphy. Bulk energy is the real issue.

So ultimately we can’t decarbonise electricity efficiently let alone get rid of diesel without more wind in the system. Governments need to recognise that.

The CIS has turned out to be neither fish nor fowl. It doesn’t provide enough confidence to developers and neither does it let the market do all the heavy lifting.

Market reforms might change things going forward but it’s like a football match, we have to fix things in real time.

So that’s where Snowy might be a face saver and Tomago support really less about Tomago and more about writing PPAs for new wind farms in NSW to support Tomago. Or I might be barking up the wrong tree on this one. But what I am very, very clear about is that if the Federal Govt really wants to get anywhere near its 80% target — a target which we all desperately support, a target that is the foundation for Australia’s energy independence and economics for the next 30 years, then wind farm PPAs and FIDs in the 1000s of MW, at least 3000, need to be announced in the next 6 months.

I have heard only the vaguest murmurings of progress. In my opinion the news will flow from the finance industry and I did see a comment of some genuine discussion. My goodness me, genuine discussion.

Now back to the good news

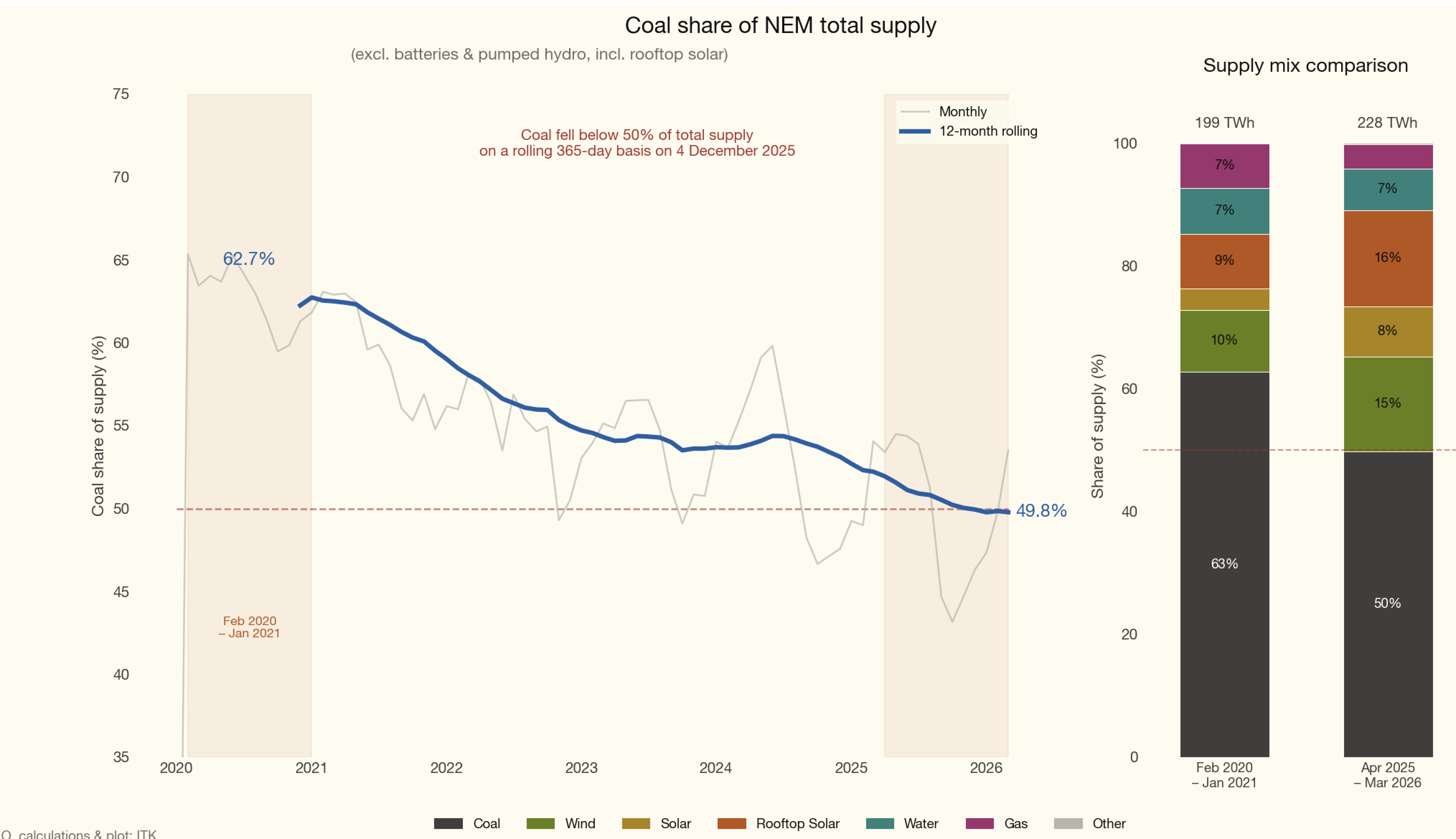

Over the past year coal generation share has fallen below 50%.

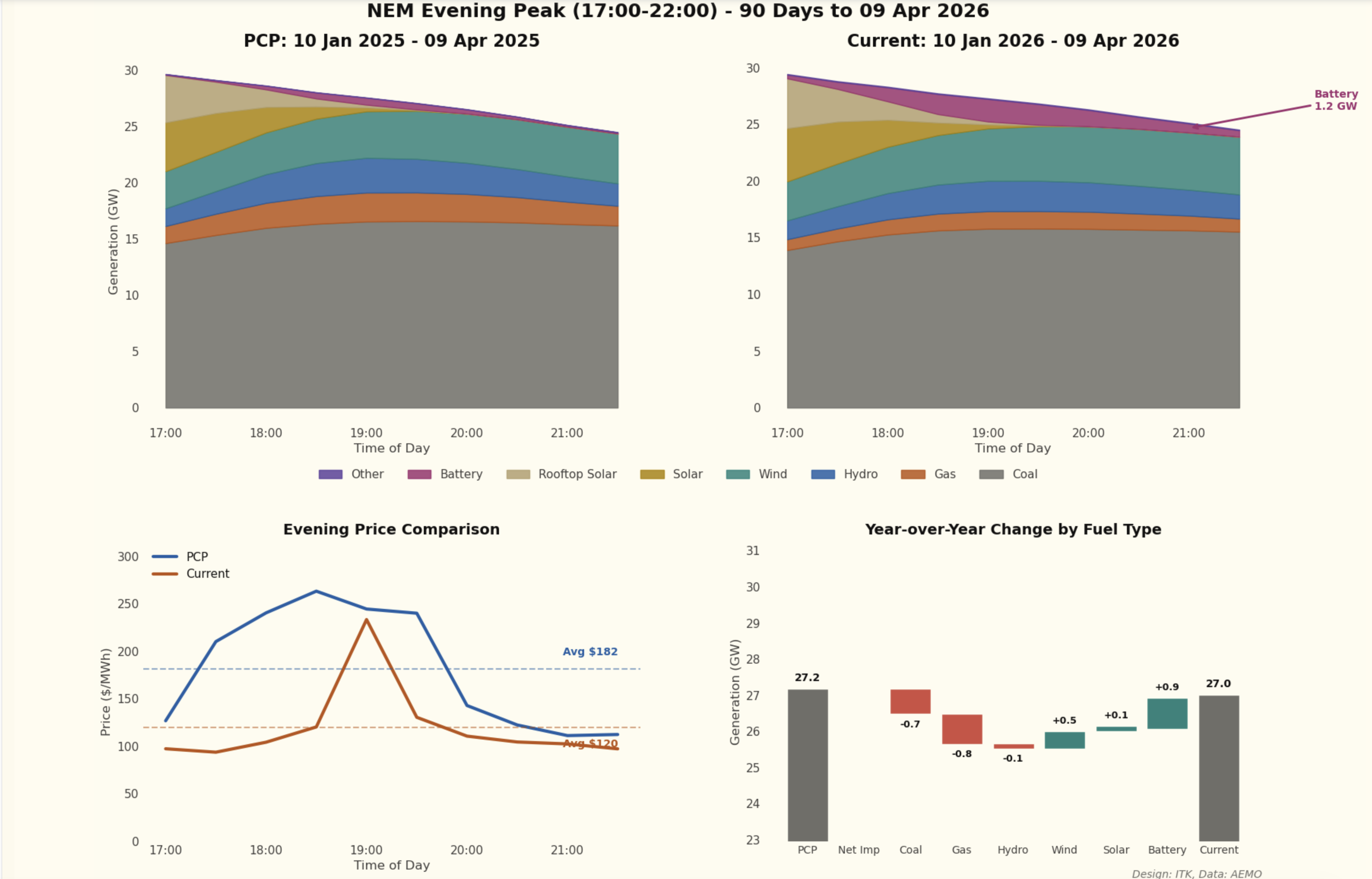

Evening peak prices are well below last year despite a decline in coal’s evening share of generation. This effect is evident in all States but is actually strongest in QLD.

Peak prices for the first 90 days averaged (weighted by region volume) $182/MWh last year but just $120/MWh this year. The waterfall chart below shows the shifts by fuel.

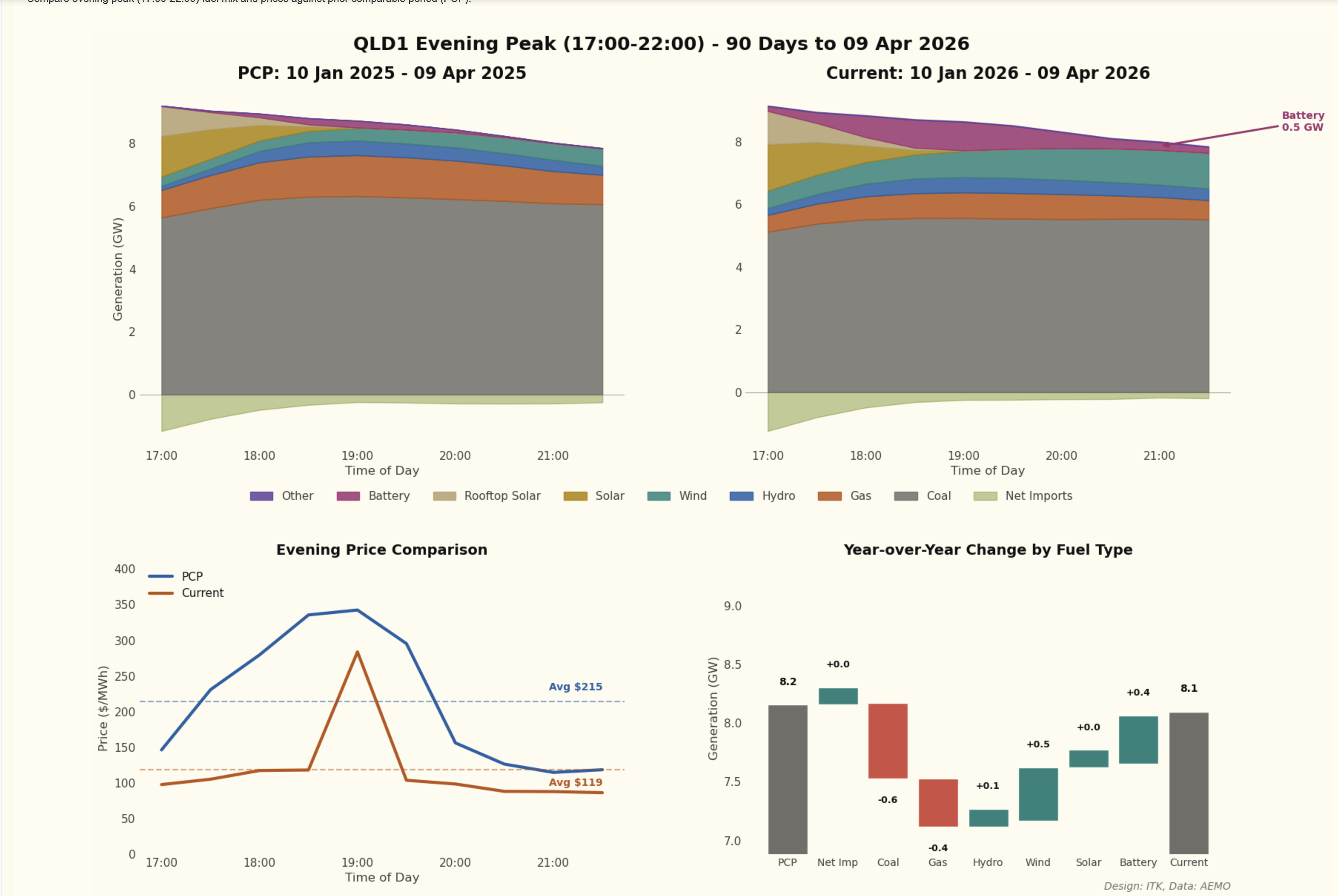

And for Queensland peak prices have virtually halved.

I need to be super careful about cause and effect here. There could well be multiple causes and I would caution that a couple of coal generators going offline could reverse these price outcomes over night.

But my view is that this year there is more competition for evening peak volumes and that’s driving prices down. It’s not just batteries although for sure they are important. Now that I think about it, there is probably more competition within the coal generators themselves because, despite say Callide C being back online, coal generators are losing volume and revenue.

Also we can’t see the impact of behind-the-meter batteries. It’s likely they are having a material impact on prices.

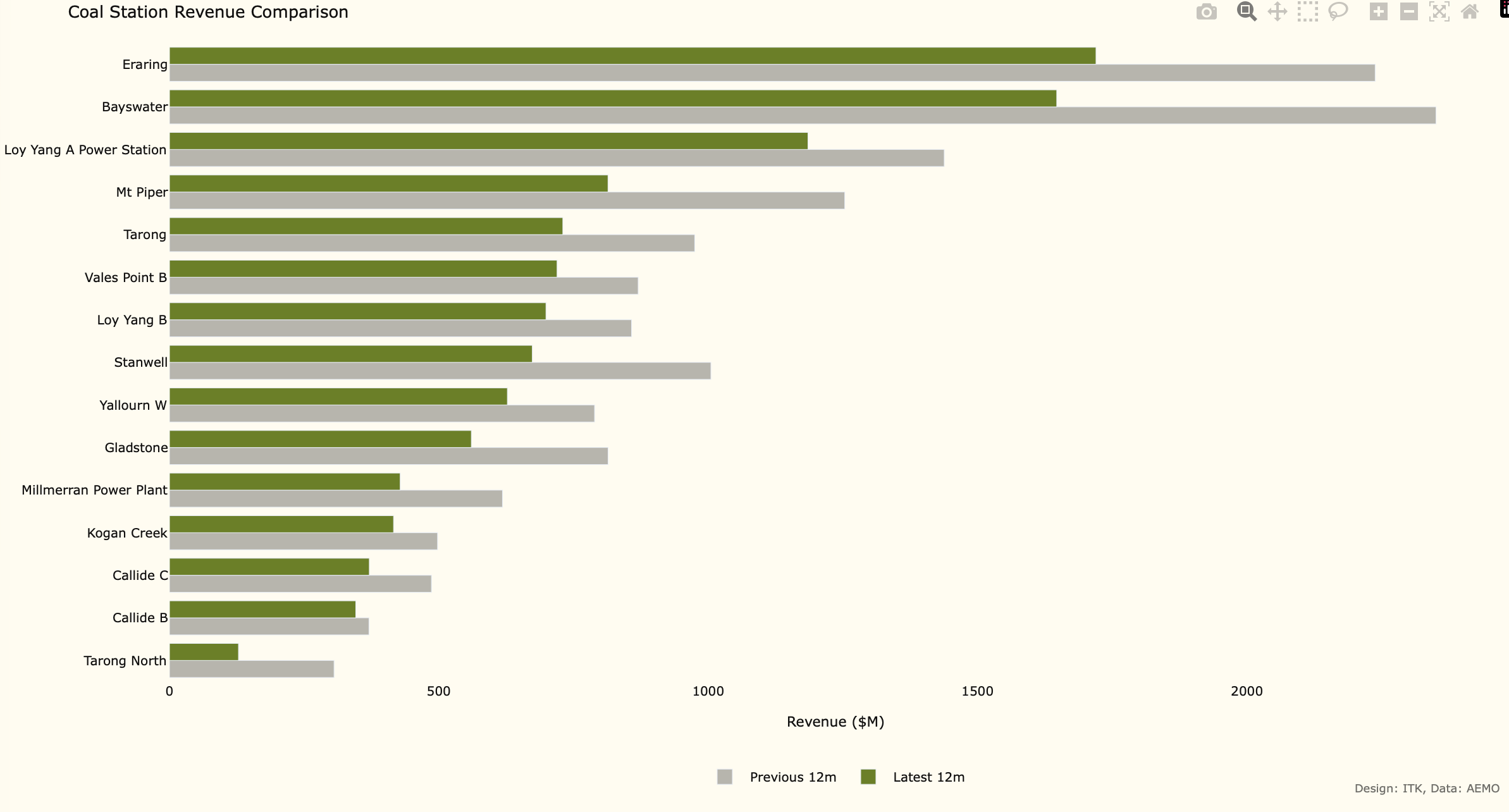

The two big NSW stations have seen greater than $500 m falls in spot revenue over the past 12 months. In isolation you can’t take too much notice of this because of hedging and portfolio impacts, but in the end the spot market is the investment signal. If the market expects low spot prices and producers expect lower spot volumes then they will reflect those expectations in hedging activities. You don’t enter a hedge with an expectation that the cost will be greater than the benefit.

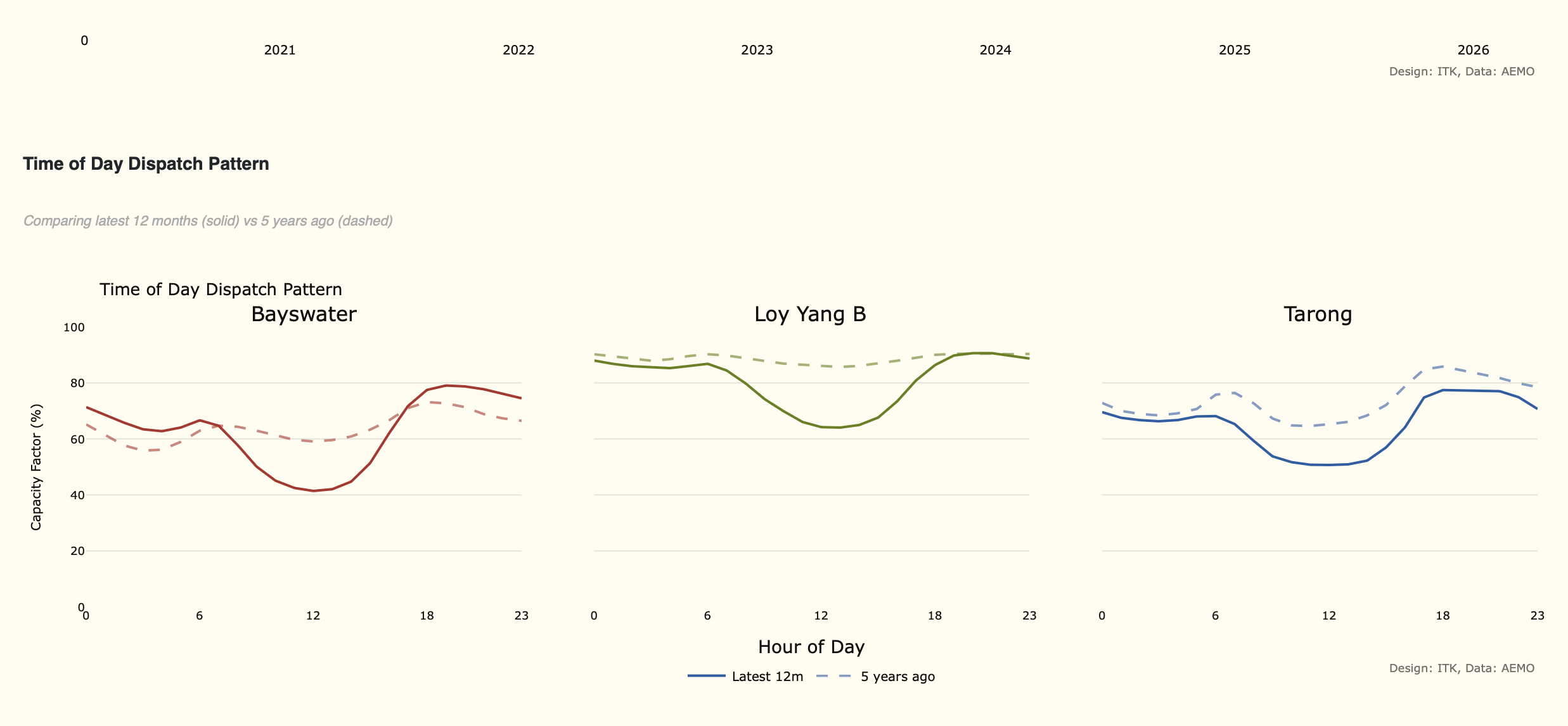

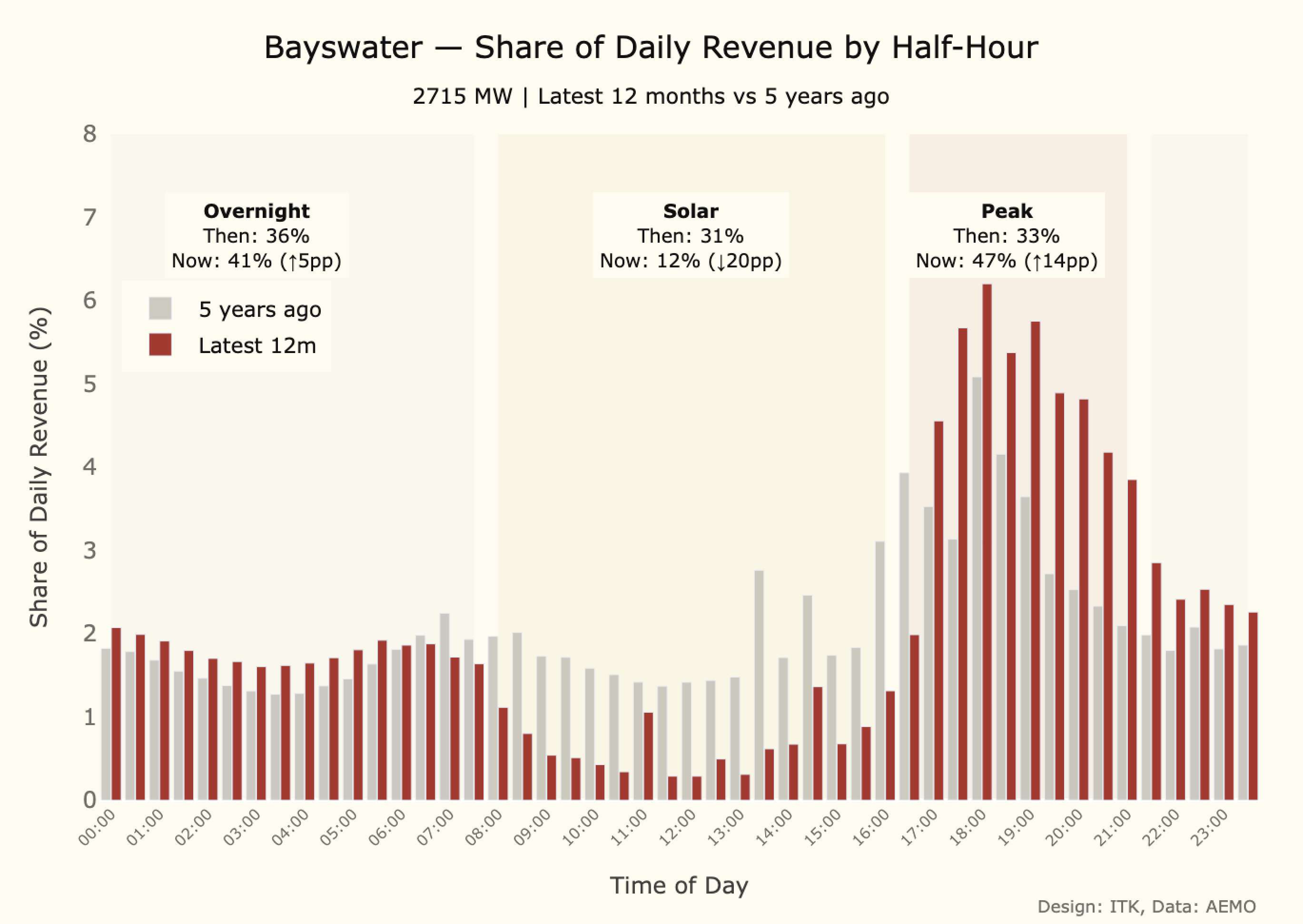

I also picked a significant coal station in each region to see how performance has evolved compared to five years ago. You can see each station now ramps much more than five years ago but for me the message is how hard Bayswater runs in the evening peak. That’s because there isn’t the wind in NSW but also the risk to Bayswater of more batteries eating into that revenue.

With the evening peak revenue opportunity already in decline, the vulnerability is clear: 47% of Bayswater’s revenue comes from peak hours.

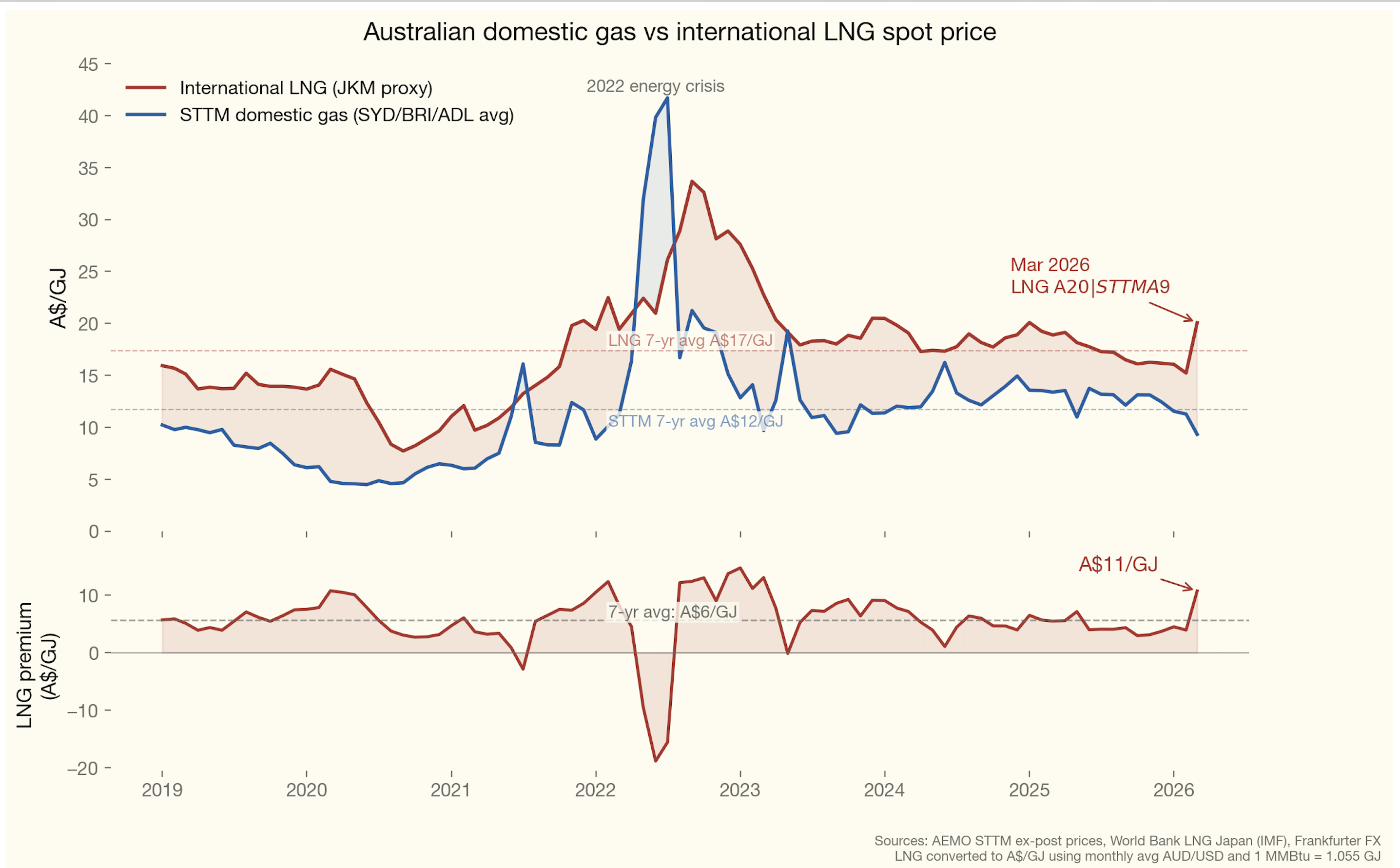

Spot gas is quiescent, particularly compared to international prices

We can debate the reasons why spot gas prices in the NEM regions have not responded to international price movements. They still might in Winter. One theory is it’s politics. Gas producers want to keep their heads down while the Govt is negotiating higher taxes. I think that’s likely.

A second reason is there just isn’t the local demand for gas at the moment. As long as coal keeps running and batteries keep commissioning, the need for gas generation goes away. In South Australia gas generation share falls most years. Only in backwards-looking Qld does anyone have serious plans for more gas generation.

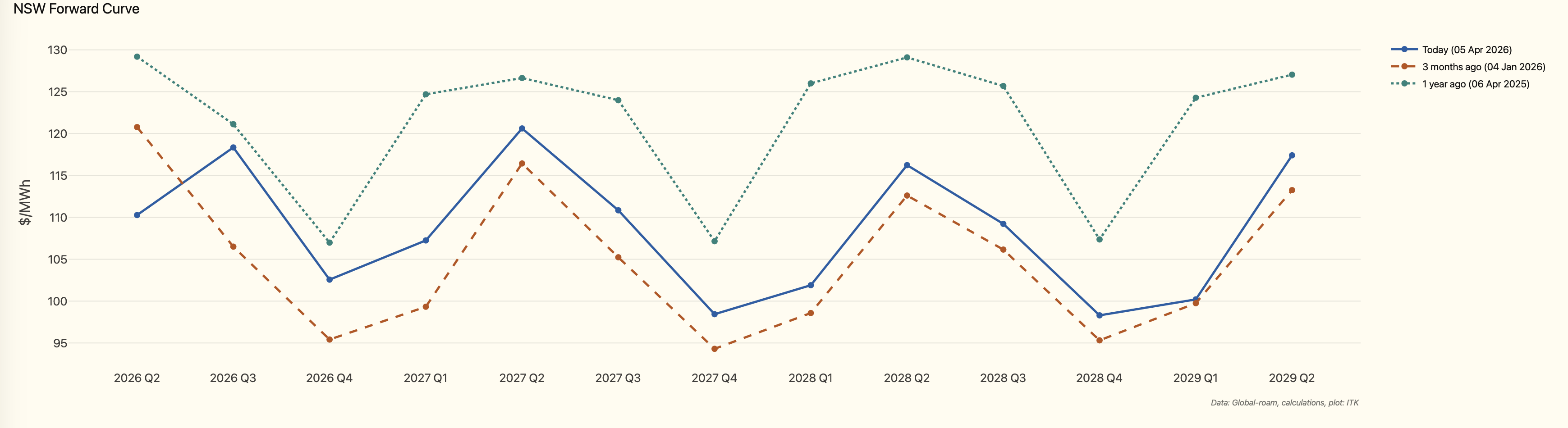

Futures are down on last year up on the last 3 months

I show NSW which probably has seen the biggest moves. In Victoria the curve has moved up fractionally v a year ago. In NSW price expectations are down $10-$15 v this time last year.

Futures expectations have to be taken as the best indicator of sentiment but best doesn’t always mean accurate. The shift in NSW likely reflects expectations that Eraring will stay open longer. This is regrettable.

New supply

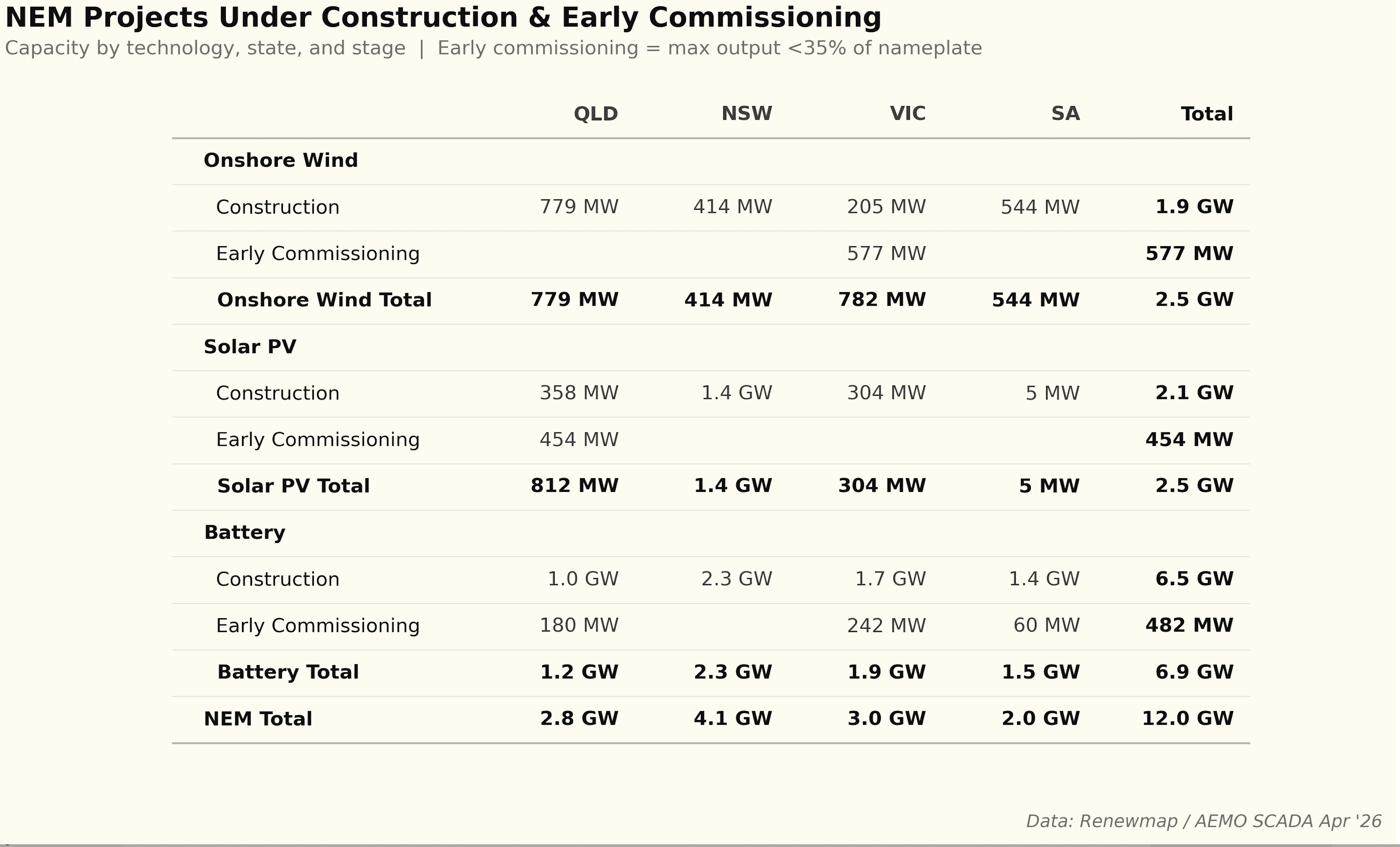

The new supply picture other than batteries isn’t going to move the dial much except perhaps in QLD. 2.5 GW of wind and 2.5 GW of solar. Come on….

Hurry up and do nothing in NSW

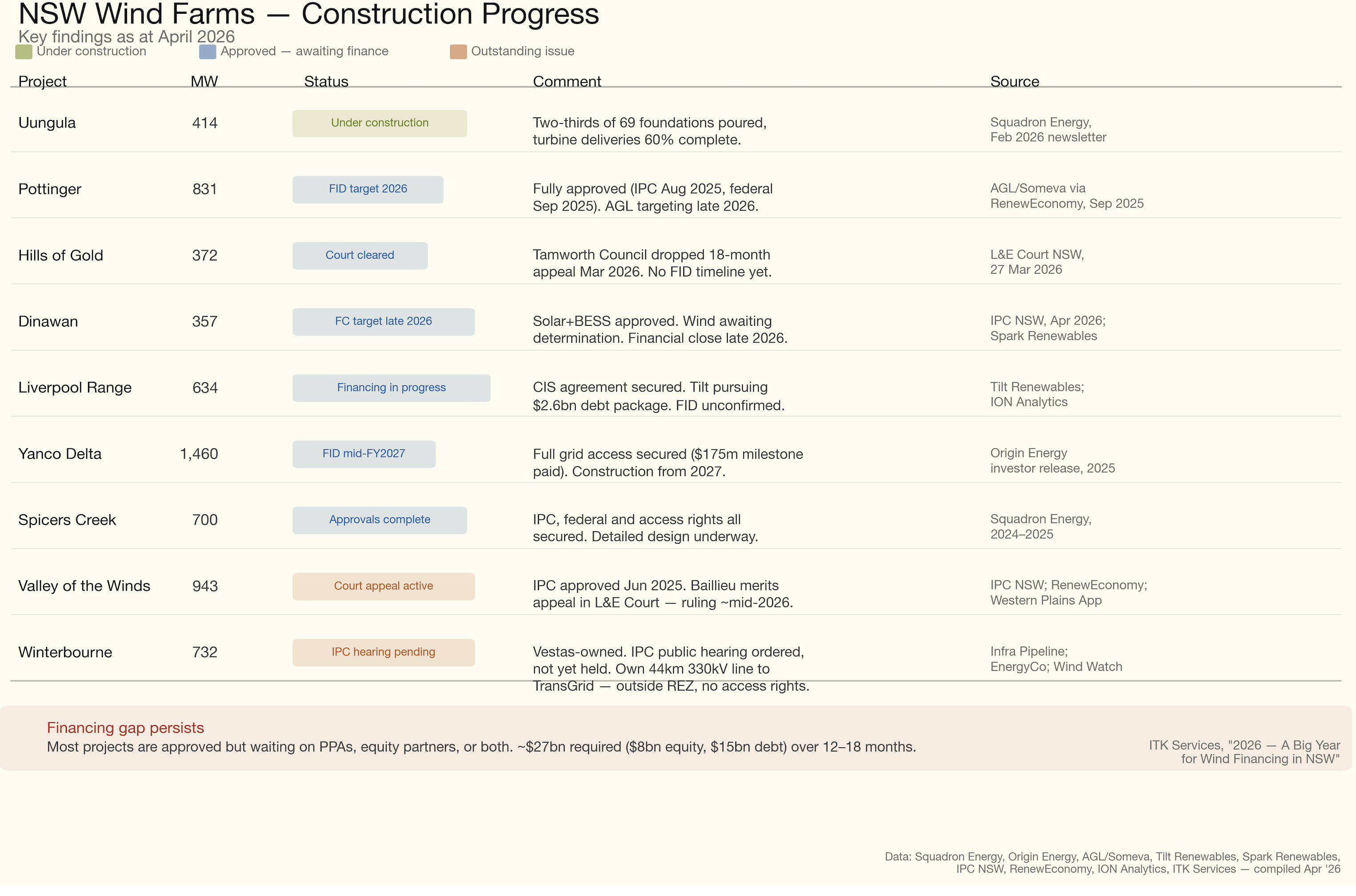

As discussed above developers sat round for years and complained about lack of transmission, slow pace of approvals. In the end none in NSW other than Uungula have got to construction with the result the transmission will be there first.

The real issue is the increase in costs so the market doesn’t clear. This note is not the place to discuss costs except to say that higher inflation is bad.

As a result the wind farms are going to be delivered years behind when they are needed raising costs for consumers and increasing the system reliability risks.

The clock is ticking.