Electrifying all road freight between Sydney and Melbourne is a no brainer - payback 2-4 years

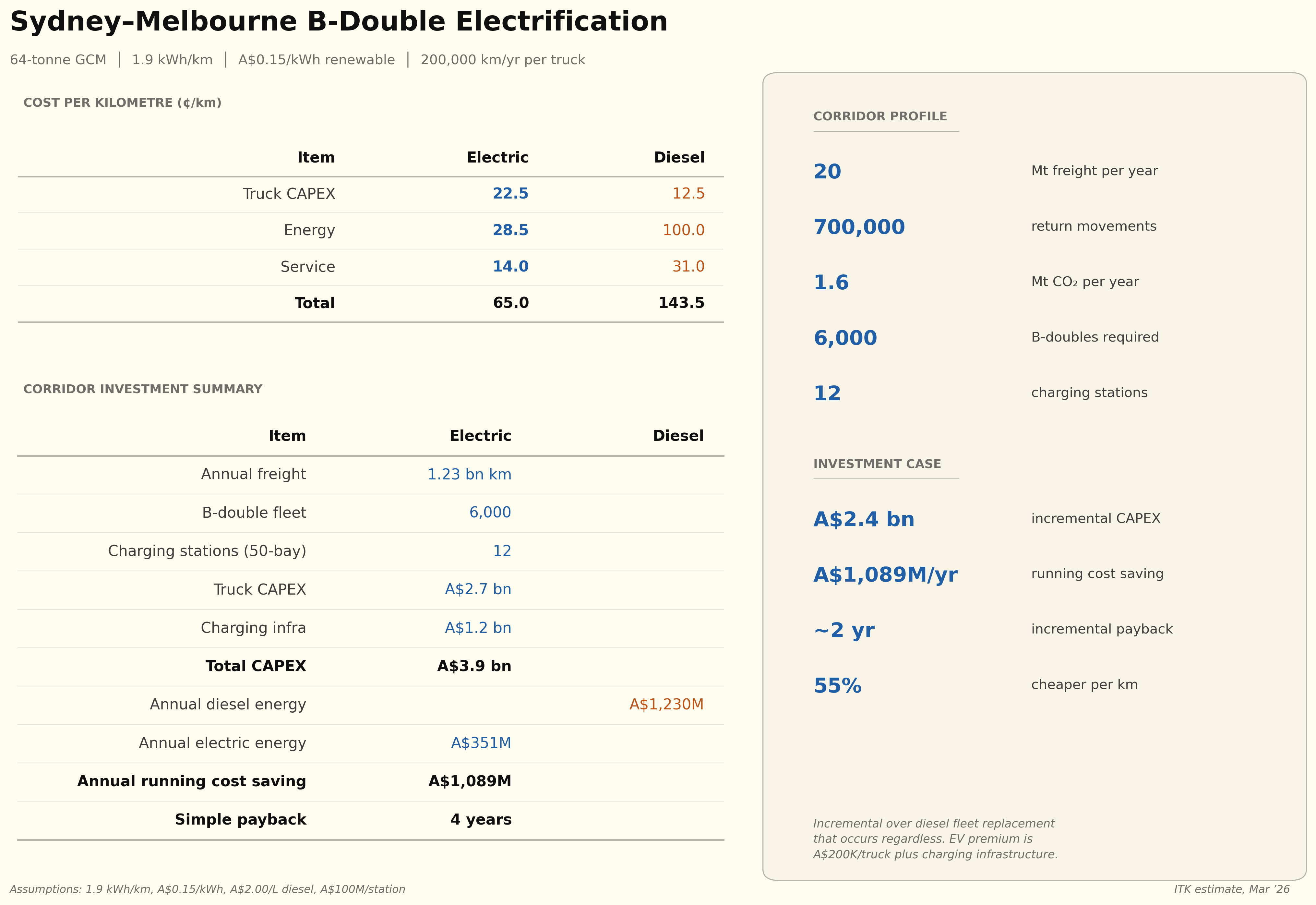

Australia has a productivity opportunity by electrifying road freight on major corridors. The economic case has become outstandingly clear over the past couple of years and there are essentially no barriers. The payback period is 2-4 years depending on whether you’re replacing diesel trucks at end-of-life (2 years) or building the fleet from scratch (4 years).

- Battery powered trucks exist that can carry 60 tonnes, purpose designed with 450 km plus of range and capable of being recharged in an hour. They are better than diesel trucks in every way: quieter, much less polluting, faster, with fuel costs one-third of diesel, better equipped inside, and less maintenance required. Drivers love them.

- An International Megawatt Charging Standard exists. That is you charge your 700 kWh battery at 1 MW, so 1 hour to charge.

- Charging stations are emerging that take up to 50 or more trucks at a time. The biggest of these by Huawei has an input power capacity of 100 MW.

About 22 mt per year of freight travels the 900 km between Sydney and Melbourne. It works to about 1.2 billion freight kilometres. When you work the fuel saving maths through, this means that if fully electrified, the industry would save about $0.9 bn per year in fuel costs plus the balance of trade , time savings, energy security and other benefits.

I estimate the capital costs to fully electrify at about $4 bn so a payback of under 5 years. But if you only count the incremental costs — that is, the charging stations and the extra cost of buying an electric semi over a diesel one — then the total incremental capex is about $2.5 bn and that’s a payback of less than 3 years.

In China about 200,000 electric semis are sold every year. It’s proven technology available pretty much off the shelf.

In other industries, eg electricity transmission, Australia has followed other countries and as a result we get caught up in the global rush when the whole world wants to do the same thing at one time. That pushes costs up, see eg transmission lines and transformers.

Australia has a very long freight distribution system, fully vulnerable to an oil supply disruption. Going early and committing fully to electrifying heavy transport and using the Sydney to Melbourne corridor as the proof of concept is a no brainer. An absolute no brainer. The economics are outstanding, the need is obvious.

If I have the sums wrong, or have missed something important I’m more than happy to have it pointed out.

Three key technological developments have made this possible.

Private sector or policy?

If the economics are as good as they seem the private sector will get there off its own bat. An opportunity to undercut the existing players by a significant amount will surely be picked up. Think Uber, think AirBnB.

However the market for the product is not consumers, it’s for those businesses like Coles and Woolworths that are major consumers of freight. There may be many reasons why a small group of large businesses are slow to embrace change.

The role of policy could possibly be a nudge. In the end it is going to take $bns of capex. Not that many $bns but capital that has to be raised. For the private sector to invest its not only the economics that have to be attractive, it helps if policy is supportive, but most of all it will come down to the business seeking to raise capital and their credibility.

What I do know is that productivity is stalling in Australia, that our goods distribution system is ridiculously over dependent on diesel and transport costs are way higher than they need to be.

The tech now exists to electrify 60 tonne double Bs

Only a few years ago the accepted wisdom was that hydrogen would be needed to decarbonise semi trailers. Since hydrogen was expensive and dangerous, the only action required was further research.

However the improving technology and plunging cost of batteries has turned that discussion on its head.

- CATL now offers a truck battery with a 1.5 million kilometre warranty.

- Windrose trucks as purpose built electrics have much lower drag coefficients 0.28, less than half a conventional semi. Windrose have just released V2 of their E700, capable of MW charging, a warranty of 600,000 km, 20% trade in , cost around Euro 250,000 and a claimed 650 km range. There are a whole bunch of innovative features in this truck and you can see a video “review” at Fullycharged. If you watch an earlier interview with Wen Han, CEO of Windrose you will see that the driver was at the centre of the design. There is a lot more to say about this 4 year old company but it’s another story. Windrose is not the only vehicle choice in this space.

- Purpose built charging stations and a settled fleet will allow for efficient charging. MW charging is the key to the success of this strategy. A 700-800 kWh battery can be recharged in an hour if the charger is fast enough. Truck drivers have to take rest breaks, mandatory rest on Sydney Melbourne is 30-60 minutes. At 60 minutes your truck is fully charged.

Really exciting economics plus the other benefits

The basic concept is that a 60 tonne truck fully charged at the outset can get to Melbourne with just one charging stop, and the charge takes an hour. Every electric km costs 1/3 the diesel cost. To do this requires the right trucks and the right charging stations. Then depending on how you count the payback is either 4 years (starting from scratch) or 2 years (replacing diesel trucks at the end of their life).

The ideas are coupled together. Because of the range only a few dedicated recharging stations are needed. These are purpose built designed to handle 50-100 MW loads running 20 hours a day. With 100 x 1 MW bays, each doing 20 charges daily, one station can charge 2,000 trucks per day. With 100 drivers on site at any time, the station can support amenities like kitchens and showers. Along the highway you could probably build a 100 MW solar farm and batteries but of course you want a 100 MW grid connection. And even 2,000 charges a day is only good for say 100,000 tonnes of freight a day. You really need about 12x 50 bay stations or 6 x 100 Bay stations. But that’s still no problem spread out over 900 km right next to Humelink.

From a big picture point of view, if this is a good idea then so is Sydney to Brisbane, Sydney to Newcastle is a doddle.

Avoiding the imported fuel cost immediately improves the balance of trade and improves our energy security.

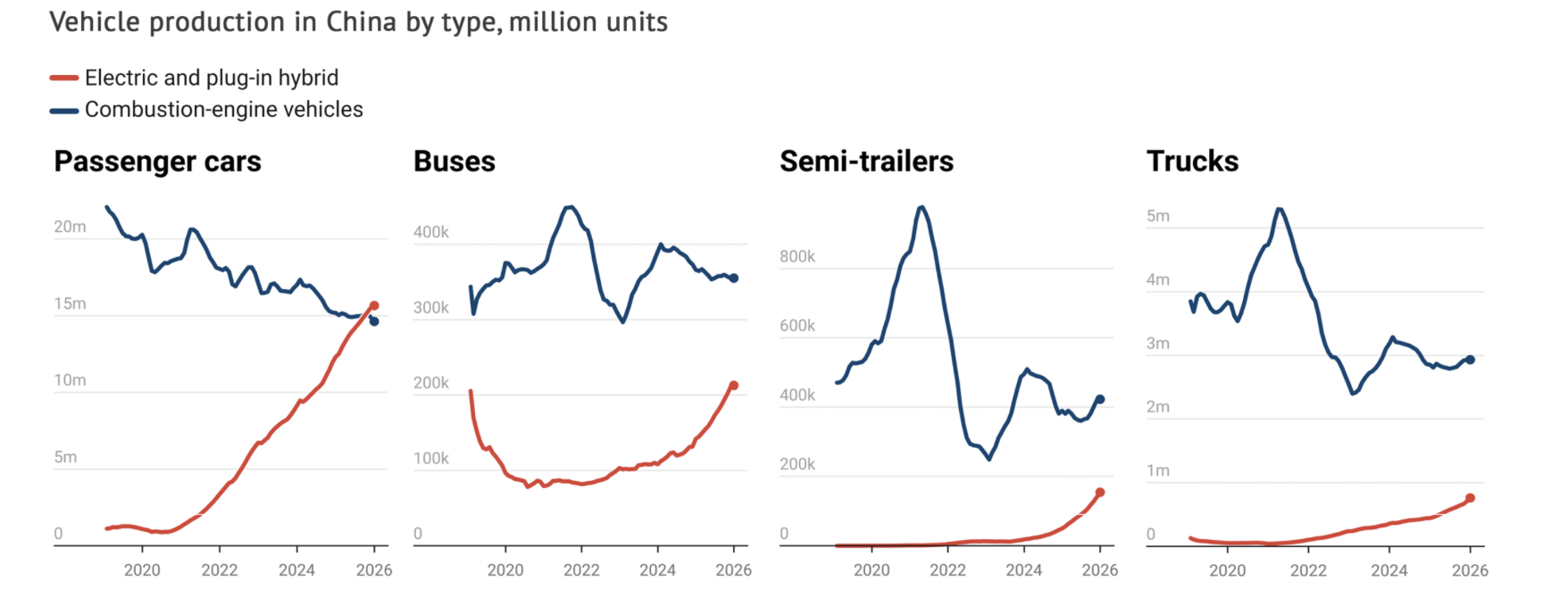

China’s already doing it and they will get better fast.

Instead of China copying the West, it’s now time for us to copy China. China’s investment and subsidies can benefit Australia as much as they benefit China. In effect, we benefit from Chinese subsidies when purchasing their EVs. If China wants to subsidize Australians buying EVs I say go for it. But in this discussion what we are buying is China’s investment in heavy electric vehicle know how. They have proved the technology up.

China now has more than 9,000 public charging stations dedicated to heavy-duty electric trucks, covering major logistics corridors, industrial clusters, ports, and mining zones (Anengjie Energy, 2025). This is an order of magnitude ahead of either the US or Europe.

You can see from the CREF visualisation below that China is now selling about 200,000 electric semi trailers a year, 1 million trucks and more than a few buses. China’s electric semitrailer share is about 33% below cars but on the rise.

Electric energy is about 1/3 the cost of diesel

Fuel represents a major operating cost for diesel trucks.

Cost per km comparison

| Electric (1.9?) kWh/km | Diesel (50?) L/100km | |

|---|---|---|

| Energy rate | $0.15/kWh | $2.00/L |

| Energy cost/km | $0.285 | $1.00 |

| Service cost/km | $0.014 | $0.031 |

| Running cost/km | $0.30 | $1.03 |

Can you get electricity at $150/MWh? I think the answer is clearly yes, if you buy enough of it and you are close enough to transmission.

So every KM an electric semi travels is $0.70 cheaper than diesel.

Electric truck capex is about double the capital cost of diesel trucks.

We are roughly talking $0.5 million v $0.25 million. If we assume the electrics are replacing diesels as they retire then its only the difference that is relevant.

The Megawatt Charging Standard (MCS)

Think I must have been asleep for the past couple of years. It turns out there is a heavy vehicle charging standard (Megawatt Charging Standard), first announced in 2018 the specification document was completed about 2024.

Unsurprisingly it turns out China is far ahead of the rest of the world but even in the USA there are 2 MW truck charging stations.

Estimated Purpose-Built Truck Charging Facility Costs

| Region | Facility | Scale | Cost (US$M) | Cost per Bay (US$k) |

|---|---|---|---|---|

| USA | Kettleman City (CA) | 56 chargers, 1 MW BESS, 3.9 MW solar | 58 | ~1,040 |

| USA | Generic 100-truck depot | 100 chargers (hardware only) | 21 | ~210 |

| Europe | Milence network (implied) | 1,700 points across 30+ hubs | 500 (EUR) | ~294 (EUR) |

| China | Huawei 100 MW hub | 126 bays (18x1.44MW + 108x600kW) | 21 | ~166 |

| China | BYD charger unit only | Per liquid-cooled unit | — | 11-14 |

The range is wide. The Kettleman City project at US$58 million includes substantial on-site generation and storage, land acquisition on an interstate corridor, and California construction costs. The Huawei facility at US$21 million is a much larger installation by bay count but benefits from Chinese cost structures and an existing industrial site. The University of Chicago’s US$21 million estimate for a 100-truck depot covers hardware and electrical infrastructure only, excluding land, buildings, and on-site generation.

Across the globe an estimate for a purpose-built, grid-connected truck charging hub with 20–50 high-power (1+ MW) charging bays is:

- USA: US$25–60 million (depending on grid works, on-site generation, and state)

- Europe: EUR 15–40 million (similar drivers, plus higher labour costs in some markets)

- China: US$10–25 million (lower construction and equipment costs, state grid support)

The single largest variable is grid connection cost. A 20 MW grid connection can require transformer and switchgear upgrades costing US$3–8 million, with lead times of 12–24 months for electrical equipment (National Renewable Energy Laboratory, 2025; TeraWatt Infrastructure, 2025). Sites with existing heavy industrial grid connections (ports, mining sites, former factories) have a major cost advantage.

Peak Charge Rates by System (2025–2026) (source:Internet research

| System | Max Power (MW) | Status | Region |

|---|---|---|---|

| MCS standard (theoretical max) | 3.75 | Standard published | Global |

| Huawei supercharger | 1.44 | Deployed | China |

| Tesla Megacharger | 1.20 | Operational (2 sites) | USA |

| ABB MCS charger | 1.20 | Shipping | Global |

| BYD Flash Charging | 1.00–1.50 | Deploying | China |

| Kempower MCS | 1.00+ | Available | Europe |

| Scania MCS (Gen 1) | 0.75 | Trucks from mid-2026 | Europe |

The practical ceiling for deployed truck chargers in early 2026 is 1.44 MW (Huawei), with the MCS standard allowing headroom to 3.75 MW as battery technology and grid infrastructure mature. Most OEMs are targeting 1.0–1.2 MW as the initial commercial sweet spot, which delivers a 20–80% charge in under 30 minutes for current battery capacities (typically 600–900 kWh for a Class 8 truck).

The Huawei 100 MW Hub

The most impressive single facility is the “Sichuan Yuanqi Xingguang Heavy-Duty Truck Megawatt Supercharging Station” in Beichuan, Sichuan Province, which commenced operations in August 2025 (Electrive, 2025; Interesting Engineering, 2025).

Huawei 100 MW Facility Specifications

| Parameter | Value |

|---|---|

| Total designed capacity | 100 MW |

| Supercharging bays | 18 at 1.44 MW each |

| Fast charging bays | 108 at 600 kW each |

| Site area | 11.5 acres (4.7 hectares) |

| Construction cost | US$20.9 million |

| Daily throughput | 700 trucks / 300,000+ kWh |

| On-site solar | ~1 MW photovoltaic canopy |

| Charge speed (3.5C trucks) | ~100 km range in 5 minutes |

Other benefits

To that we can add:

- Carbon benefit: A one way trip in a B Double Sydney to Melbourne is about 1.4 kg of CO2 per km. For 1.2 bn tonne km required to transport the 22 million tonnes of road freight between Melbourne and Sydney per year thats about 1.7 million tonnes of CO2.

- Driver benefit: Drivers can suffer hearing loss and are exposed to diesel health issues.

- Time savings: Because of the extra power going up hills you will likely save 30-60 minutes each way. If we value driver time at about $100/hour with on costs the actual wages savings per year are quite material.

- Other travellers avoid being stuck behind semis because now everyone is travelling at the speed limit.

- Noise is hugely reduced: If you’ve ever been in a motorway tunnel with a semi you know how noisy they are.

Double Bs

The Double B configuration is common. Of course, there are many different semi configurations doing Sydney to Melbourne.

Tonnes and cubic volume

Transport like any topic has its own traps for space cadets. I was thinking about the maybe 24 mt of Melbourne to Sydney freight and how many trucks and truck km are really needed. Probably a better way to think about it is 20 ft containers. A B double takes 2. A 20 ft container can carry around 24 t of payload but it’s really the cubic volume that drives it. If you think about groceries with beverages, canned goods, packaged dry food and so on it averages about 300 kg/cubic metre and a 20 ft container has a volume of about 33 cubic metres. So the typical payload is more like 10 t than 24 t.

Battery weight

A 700 kWh battery adds about 4 t to the tare weight of a semi compared to a diesel. Much better to spread that weight over a B double.