Nelson’s blind eye

The Australian energy market faces a fundamental problem: major gentailers won’t invest in renewable energy because they expect spot prices to fall below the levelized cost of energy (LCOE) and because they can’t control wind and solar output. After years of watching gentailers avoid wind and solar PPAs while eagerly building batteries and gas plants, it’s time to acknowledge reality. The Government should abandon complex schemes designed to preserve private sector involvement and instead directly fund renewables through vanilla Contracts for Difference (CFDs).

It’s been clear for years and years that the major gentailers don’t want to own, finance or write PPAs for wind and solar. The gentailers will nickel and dime any CIS or Nelson style contracts until the private sector’s role is meaningless.

Although its easy to be negative about Gentailer motives for not writing PPAs I have come to the conclusion its (1) because gentailers have formed a collective expectation that average spot prices for wind and solar (prices received from the pool market) will be lower than LCOE (prices required to recover investment, and therefore the PPA price a developer will require). (2) Gentailers cant really apply any market power to wind and solar by making dispatch/withhold decisions in the same way that they can will all forms of dispatchible power. There are other factors as well.

Will solar and wind farms earn LCOE?

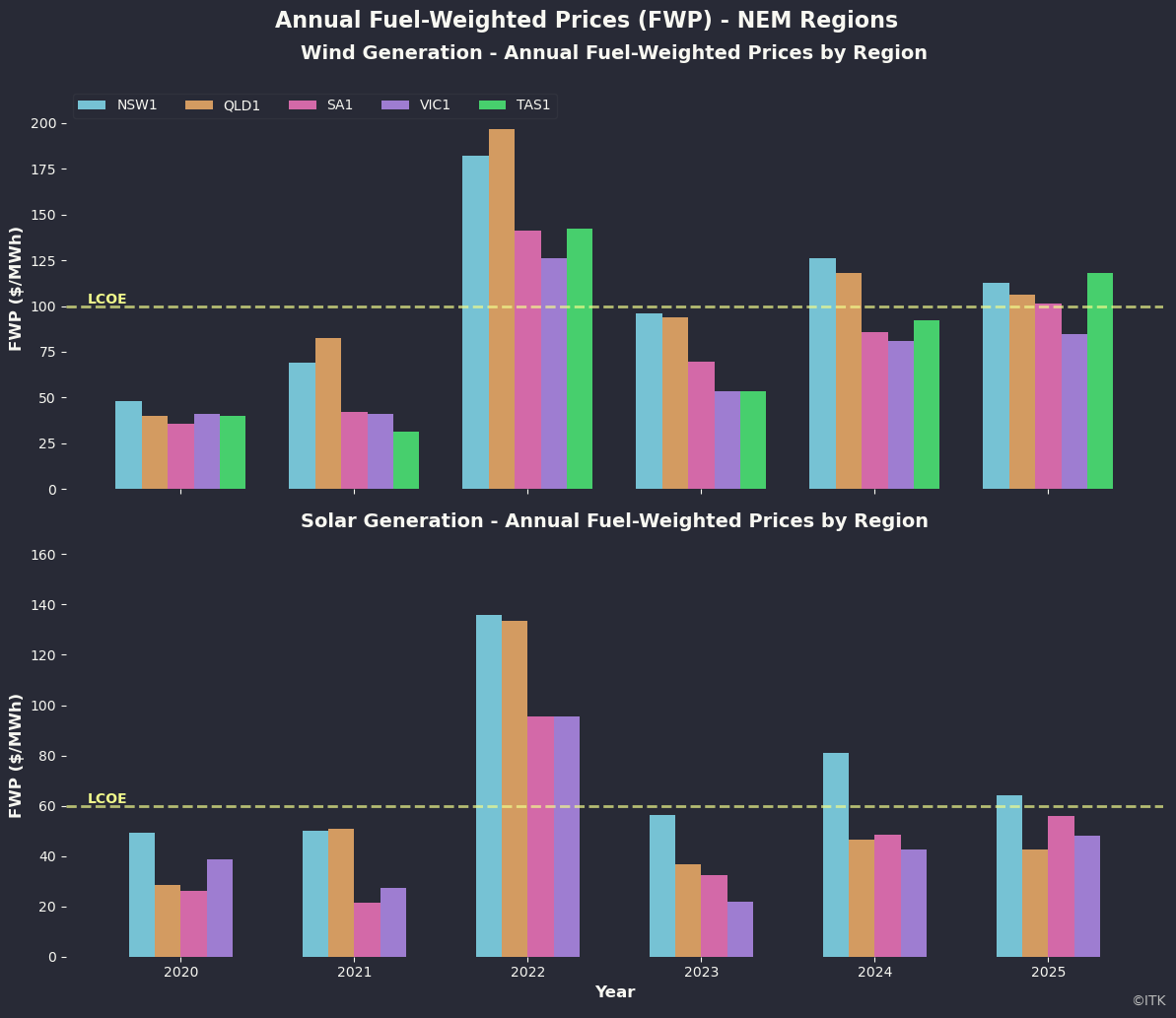

The following plot is perhaps overly simple. It takes the calendar1 annual average fuel weight price2 and shows that compared to a single LCOE. The LCOE is ridiculously simple. It’s just set at $100 flat for wind and $60 for solar. Who cares about costs and interest rates etc.

So the question is, if you are a gentailer do you think you will recover LCOE? In answering the question your CFO would firstly observe that:

- Historically you would also get an REC. Your answer as CEO is yes but RECs are expiring, price depends on voluntary surrender and that’s risky;

- By and large regions where spot averages exceed my arbitrary LCOE either have low supply relative to demand eg NSW, or the wind and fuel penetration is relatively low eg wind in QLD.

- I don’t show the data but as you might expect solar price relative to the average price have been declining consistently over the past five years. The percentage of the average flat load load price that a fuel receives is the capture rate. Solar was capturing 60%-90% of the flat load price in 2020 but now its pretty much at or below 50%.

My conclusion is that based on history you could justify a wind farm PPA but you’d have to be lucky with solar, or at the least be dependent on RECS. Or to put it the other way, if you were a large retailer you wouldn’t pay much to hedge wind bought from the spot market and you’d rather buy solar out of spot than be paying some developer.

However it’s the far trickier prospects for average solar and wind achieved prices over the next 25 years that are where the investment decisions will be won and lost.

I look hard at the forecasts from ITK’s price forecasting model and I think its quite reasonable to think wind and solar capture rates can fall going forward. As the share of wind in the total energy system increases it’s likely that when the wind blows the price will be low and vice versa. You can change that by putting more storage in but the more storage then the lower the return on that asset.

Other Contributing factors

These include:

- Cost of wind development has increased sharply so the wind PPA market doesn’t clear. I think the evidence for the increase in the cost of wind is abundant and it’s well known that rapidly increasing costs cause sticker shock and cause deals to be delayed. Contrary evidence is that Gentailers stopped taking an interest in wind long before the big Russia induced cost increases.

- Return on equity for stand alone utility solar has been compromised by initially underestimated competition from the rooftop solar market;

- The absence of an increase in the RET obligation removes the stick that drove gentailers to sign PPAs. Origin for instance had a long standing policy of having enough REC cover for its mass market load, and an increasing REC percentage would have led to them signing the bare minimum of new PPAs required.

Still these are only my ideas. If you look at the history ORG has never had any interest in renewable energy Grant King used to sneer at the returns while blowing money on high return high risk projects. Michael Fraser and Jerry Maycock took AGL from being a leader in the Australian wind space to Australia’s largest carbon emitter. Maycock had already shown at CSR that he was a very poor judge of the what was in shareholders’ long term interests. Fraser simply didn’t care that much. I doubt if he understood carbon policy and risks, if he did he was certainly prepared to sacrifice long term credibility for a short term deal. AGL have never recovered, because the investors have little interest in a short life coal generation portfolio where the present value declines 10% a year. If the QLD govt had half a brain it would realise the same thing although the discount rate might be a bit less. Investors need something to believe in.

Gentailers have been on a buyer’s strike for years

Origin Energy

Origin has not announced any wind or solar PPAs in the past 5 years. Zero, zilch nothing. Its last purchases were for its own development Stockyard Hill where it wrote a PPA in order to make the project saleable. And before that Darling Downs Solar farm.

Origin is also kind of playing the NSW Govt for a fool. It has a no risk insurance policy to get a return on Eraring if conditions go against it and at the same time if electricity prices are high, well its carry on Sergeant Major.

Origin will point to its investment in Delta Yanco wind farm for which it may end up paying as much as $300 m but that’s just one project. To replace the 15 TWh of annual output from Eraring needs say 5 GW of wind or more of solar.

AGL

AGL’s last PPA was with Rye Park to take 45% of output where again the deal was done with its 20% owned investment Tilt Energy who owns the project. AGL is believed to have first rights of refusal over any Tilt Development a good prize for a 20% investment. Those first rights may only apply to projects that existed at the time PARF acquired Tilt and renamed itself. Nothing has ever been disclosed. Before that AGL did a deal with Maoeng in 2017

AGL is just as bad. The company had the nerve to print its renewable share of generation was around 20% in FY25. This at a time when including rooftop solar the broader NEM is at close to 40%.

I have also long argued that it’s such a hopeless cultural job. Where is the marketing appeal in the product offering?

In AGL’s case coal generation is around 30 TWh per year earning probably around $1.1 bn of ebitda, maybe more, maybe less, but in terms of cash flow its certainly a lot less because around $400-$500 m of maintenance capital expenditure is being spent a year. So at that rate and with AGL’s coal generation current scheduled to completely close within 10 years the company will have spent maybe $4 bn on completely dead assets with no future. I get that there is a positive NPV in the process but I still can’t help thinking what a waste.

Energy Australia

Surprisingly Energy Australia has announced two deals:

- 40% or around 345 MW of output from Golden Plains stage 2

- 30% of Kidston wind farm (about 77 MW). However I don’t believe this project has reached FID and has been reduced in size

So I don’t know what readers think but for my money these big gentailers have essentially said to the public “screw you”. That would particularly be the case for Origin. It’s true you can cut them some slack because of the aborted Brookfield takeover but the fact is Origin despite many fine words has never really been there for wind or solar. Far better to go successfully gambling on Octopus Energy than to roll the sleeves up and offer Australians the products they actually need.

The contradiction: Gentailers eagerly invest in batteries and gas

The most obvious evidence is batteries. Each of Energy Australia, AGL and Origin are happily building batteries on balance sheet and also contracting output from other batteries. On balance sheet batteries have a life of say 20 years, and increasing. This clearly shows the big gentailers are happy taking tenor risk. You can bet a bunch of money that if Snowy had spare balance sheet capacity it too would be building batteries.

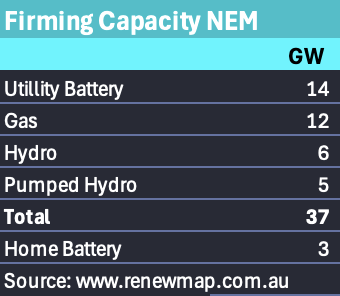

The following two tables summarise the non coal firming power in the NEM, the batteries total uses Operating, construction and commissioning total. Batteries are now the biggest part of the total. Home batteries are great and I’ve based my total here on 0.5 m houses with 5 Kw of power, but you can make your own number up, it still won’t be as important in the overall scheme of things as utility batteries. Except, and providing not run by a big gentailer VPP they may help with peak pricing competition.

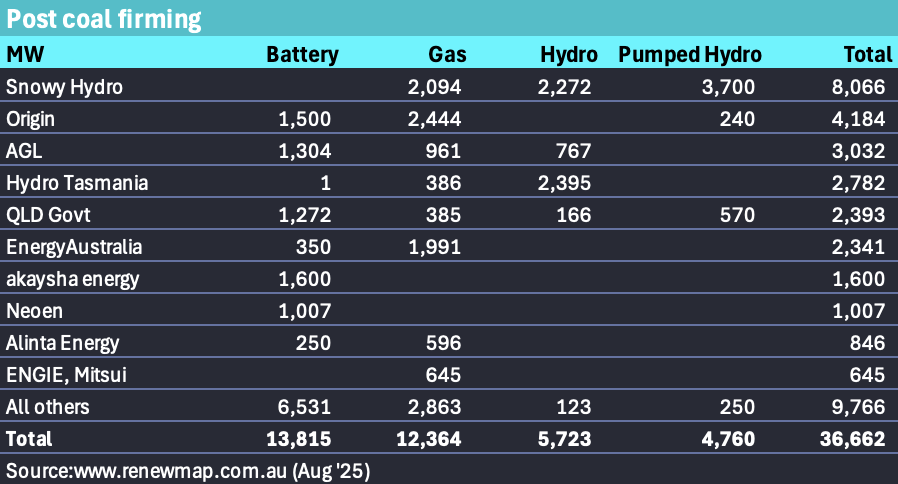

In terms of peak prices, an area the Nelson review might usefully have spent some time discussing, we can see that already the top 5 providers have over 50% of the post coal firming power. And that AGL and Origin in particular have been falling over themselves to make sure they retain as much control of the post coal firming market as possible. I make it over 3000 MW of either development funding or PPAs they’ve signed up for. I should also include the Genex pumped hydro in in the Energy Australia total and no doubt there are other PPAs I’ve missed. On balance stuff I haven’t accounted for would I am guessing increase the market share of the large gentailers and further make a nonsense of the Nelson Committee view that big Gentailers see the future as too risky to commit to.

Secondly two of the big gentailers have built gas generators in recent years. AGL with Barker’s inlet and EA with Tallawarra stage B

Looking further back, and perhaps fundamentals have changed although in this regard I would argue not, each of AGL, ORG and EA was happy to own long term coal generation and as far as I can tell happy to take the tenor risk of operating it as long as possible.

Finally the gentailers haven’t even been signing short term PPAs.

CEO perspectives reinforce the pattern

Frank Calabria’s views can be summarised as “more gas”. I quote from a Calabria authored AFR article headlined “My policy pitch” in April 2025:

The most pressing energy policy for an incoming federal government, within the broad review of the National Electricity Market (NEM), is a framework that provides clear investment signals to market participants.

One of the most pressing issues is to value all the services needed for an efficient and resilient energy system and ensuring investment in the right mix of technologies. Gas generation will continue to play a pivotal role in stabilising the energy system and keeping the lights on under all weather and supply scenarios, yet current policies fail to provide any incentive to invest in this technology.

You won’t find wind and solar mentioned by Calabria in that article except to note that some wind and solar has been built, arguably despite ORGs best attempts to avoid it. There is no suggestion from Calabria that wind and solar are a good idea, or that wind and solar policy is needed or that even if there were such policy that Origin would have any interest in it. It’s the usual complaint about gas, without ever acknowledging that ORG has gas generators in every NEM state bar Tasmania. In other words it is entirely self serving. That’s fair enough it is Calabria’s job to be like every other CEO and just talk the book. To expect more is unrealistic. And so we get it. Calabria’s policy pitch is “More gas”. That is the pitch from the leading Gentailer CEO. It’s the sort of message that I find depressing because ORG could be so much better. People look up to the CEO of Australia’s leading gentailer, employees, schoolkids, uni students, the media, the public, investors. People who look at climate change and see its long term danger and what does our fearless leader prescribe? “More gas”. Great. How about a contrast with say JFK “ask not what your country can do for you but what you can do for your country”. I really doubt the answer to that question at this time is “more gas”.

As detailed below though, Calabria is a realist. Gas provides a bigger oligopoly guarantee than batteries but if it has to be batteries well ORG along with AGL and EA will be there. Only Snowy is left out committed to Snowy 2 and no more funding available. The point is Calabria’s view is shared. Gentailers don’t want wind and solar and until the Federal Govt internalises that it will keep coming up with schemes that would help the private sector if the private sector was interested. But it isn’t.

The Nelson Review’s (deliberate?) Misdiagnosis

I quote from the Nelson review executive summary p 11.

Historically, significant investment in electricity infrastructure has rarely occurred without some form of government support. The most prominent example of this government support has been the Renewable Energy Target (RET) which has historically delivered the vast majority of investment in small-scale and large-scale renewable resources. However, policies such as the RET have substituted coal-based energy with renewable-based energy, without any additional requirements to provide the other services consumers need, namely:

• Shaping: Moving electricity to the time of day it is needed

• Firming: Long-duration dispatchable capacity to deliver extra energy as needed

• Essential system services: Securing and stabilising the grid with a range of services, including frequency control, voltage regulation, system strength and inertia.

The CIS and state-based interventions such as the New South Wales Electricity Infrastructure Roadmap are the current policy instruments for de-risking private investment. But these policies sit adjacent to, rather than within, the market’s structure which is articulated through the NEL and NER.

In the absence of a nationally consistent replacement for the CIS, investment will be driven by state- based schemes, resulting in a more complicated and fractured investment landscape, which may fall short of what the system needs.

The first and most persistent of the barriers to new investment is the ‘tenor gap’: a mismatch between the long‑term contracts needed by sellers to finance capital-intensive assets (often 10 to 30 years) and the short-term contracting of buyers (typically three to seven years). This tenor gap is driven by a broad suite of uncertainties – technological, regulatory and demand-related.

Not to put too fine a point on it I regard this as largely garbage.

The evidence clearly contradicts the “tenor gap” argument. As shown above, gentailers are happy to take 20-year risks on batteries and gas plants. The idea that gentailers don’t have any certainty about a load into which to sell PPA output is also unsupported by any evidence in the Nelson review. I mean just think about it:

“the tenor gap is driven by a broad range of uncertainties - technological, regulatory and demand related”

Personally I’d like to see the committee adduce some evidence as to those uncertainties, which as far as I looked, was not provided. But equally the fact that market structure, ie a big fat oligopoly of coal owning gentailers correctly aiming to maximise NPV of their assets is completely ignored. And I think this is unreasonable and makes it hard for me to take the committee report seriously.

You can also read in the above quote the review authors’ fondness for the LRET scheme instead of replacing it with the CIS.

Since the Government has to do the financing due to Gentailers being unwilling let’s stop pissing round.

The only way to get to Gentailers to write wind or solar PPAs is by some form of mandatory share of renewable energy. This could but won’t be a simple mandate, but historically was done via the LRET scheme and REC certificates. Since the Nelson Committee has been given the word that certificates are out this leaves only one choice. Get rid of any pretence about the Gentailers. The Government is going to be on the hook so it might as well do the job properly. And the, to me, obvious way to do that is via vanilla CFDs with say a 20 year term. If done on a regular schedule the Government will end up paying on average the correct price. Developers still take financing, construction and operational risk. Once built the assets can be resold into an infrastructure fund offering infrastructure style returns.

In this scenario the Government’s problem is it will pay LCOE but receive spot and that is exactly what Gentailers have been seeking to avoid. However if the Government finances all the wind and solar from this point it will end up in control of the forward market and gentailers, who ultimately do need forward cover will have to come to the Govt for forward contracts. This is similar to what the Nelson review suggests except it cuts out all the nonsense about the private sector contracting short and just lets the Govt get on with providing the requisite guarantees financiers need to commit.

The CIS scheme, I think is a pretty good scheme, but its designed with the idea that wind and solar developers will need not just a CIS contract but a contract with, most likely a gentailer, to provide the equity return on the project.

The Nelson review has some variation on this where once they work out what the contracts actually look like they then require developers to get a short term PPA with your friendly gentailer.

But why do any of this? Gentailers have made it abundantly clear they don’t want to be involved with wind or solar. Because they are unwilling they will have to be forced into it and that’s just going to delay the whole process.

Both the CIS and the proposed Nelson Contracts represent attempts to provide Govt assistance but preserve the market. No matter how cleverly designed such schemes inevitably lead to the Govt picking winners according to more or less disclosed criteria and bid prices.

The effect is the exact opposite of what the Nelson review wants, namely liquidity and transparency.

Nothing wrong with a good old vanilla CFD

CFD PPAs as issued by the ACT and Victorian Governments are contracts where the buyer, in this case the Federal Govt agrees to pay a fixed price per unit of energy produced by the project developer over the contract period, the longer the contract the lower the price required.

They fell out of favour because (1) they represent Govt intervention, (2) The Government might agree to pay too much. Subsequent schemes like LTESSAs and CIS were more designed to de-risk projects from the developer’s perspective whilst still leaving as much as possible to private negotiations in the contract market

But I would argue that without some element of compulsion the gentailers just aren’t there.

So instead of a CIS or some fancy new contract lets have the Government just issue plain old vanilla CFDs.

If the spot price is below zero then that can be excluded.

By holding auctions regularly say every 3 months a form of “dollar cost averaging” can be achieved meaning that on average the Government will pay the appropriate market price. Competition amongst developers to get a PPA generally ensures that prices are appropriate.

Clearly the Government has to decide on the appropriate technology mix of wind and solar and maybe firming but that is no different to what happens now.

The energy can still be traded in the spot market. Of course the Gentailers will then have to buy out of the spot market, or they can compete with the Government for new supply, or they can as the Nelson Committee wants negotiate to buy contracts from the Government.

What I propose is not all that different, as far as I can tell from Nelson style contracts except there is less BS. Of course there have to be penalties for not starting any contract awarded by the due date.