Fuelled by the Australian Sun

Interested parties need to formalise their approach to develop policy and solutions for EV trucks. There are many excellent reasons to do so: economics, national interest, and plain old keeping up. There is lots to do and not much time. If we do it right there will be jobs, lower costs, a happier, healthier, safer and less polluting trucking industry. Australia can replace $40 bn of net imports ($60 bn gross) — the equivalent on the trade balance of our gas export industry.

More torque

Australia has a strategic imperative to find industries we can grow. Solar energy and wind are two of the most basic industry inputs we have.

Australia has been struggling to find a way to take advantage of our solar and wind resource, particularly a way to use them to replace coal and gas exports.

Reducing oil imports has the same effect on the trade balance as increasing exports, and it reduces our strategic vulnerability. The bigger diesel is as a share of costs, the bigger the advantage of replacing it with solar power via batteries. And every Australian wants to consume more things that are home grown, made in Australia.

Solar powered transport, via batteries satisfies all those things. This is recognised not just in Australia but, I’d argue, in every oil-importing country. We need to move fast in order not to be left talking when everyone else is already in motion.

However we don’t want to rush in. We do need to plan properly, set goals and then we can have a race to see who does it best. The winners get the prizes.

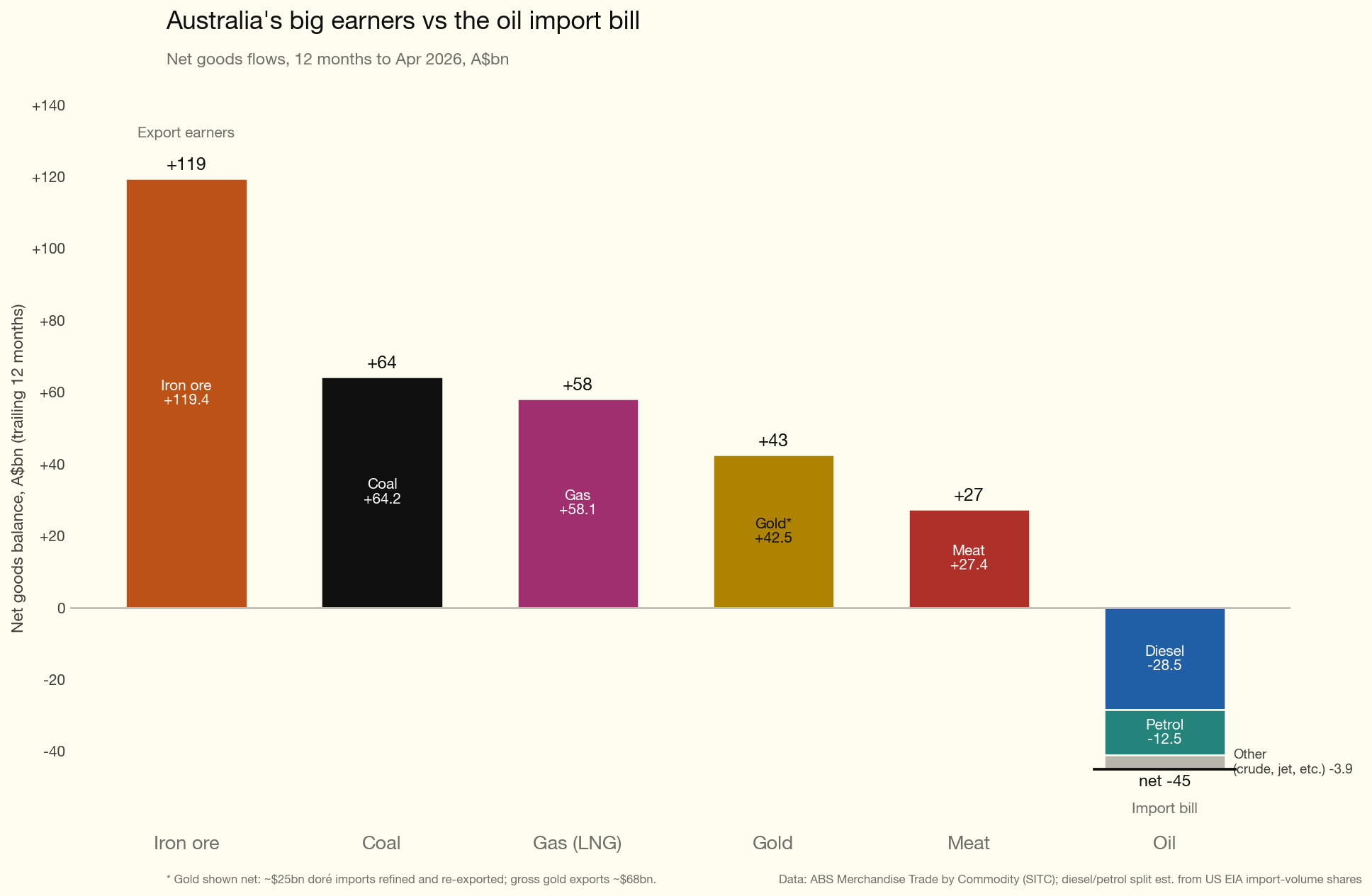

Oil’s significance in Australian trade flows

Note that the above shows traded goods only and also ignores many other imports. It does show our major exports, and the point of it is to show the significance of oil relative to coal and gas exports. Oil is shown on a net basis. We do export oil products, but they are in decline. In my opinion even our coal is less competitive than it used to be on the world market.

The vast majority of petrol goes to passenger cars. Policy for passenger cars is already well developed. It’s worth noting that investment in green iron should also be a national priority, but it’s also obvious it will require BHP and RIO to be onboard, and that is a thankless task. Also, the required investment is next level.

The plot makes clear though that whereas consumers and voters care about cars, from the economy’s point of view it’s diesel that matters.

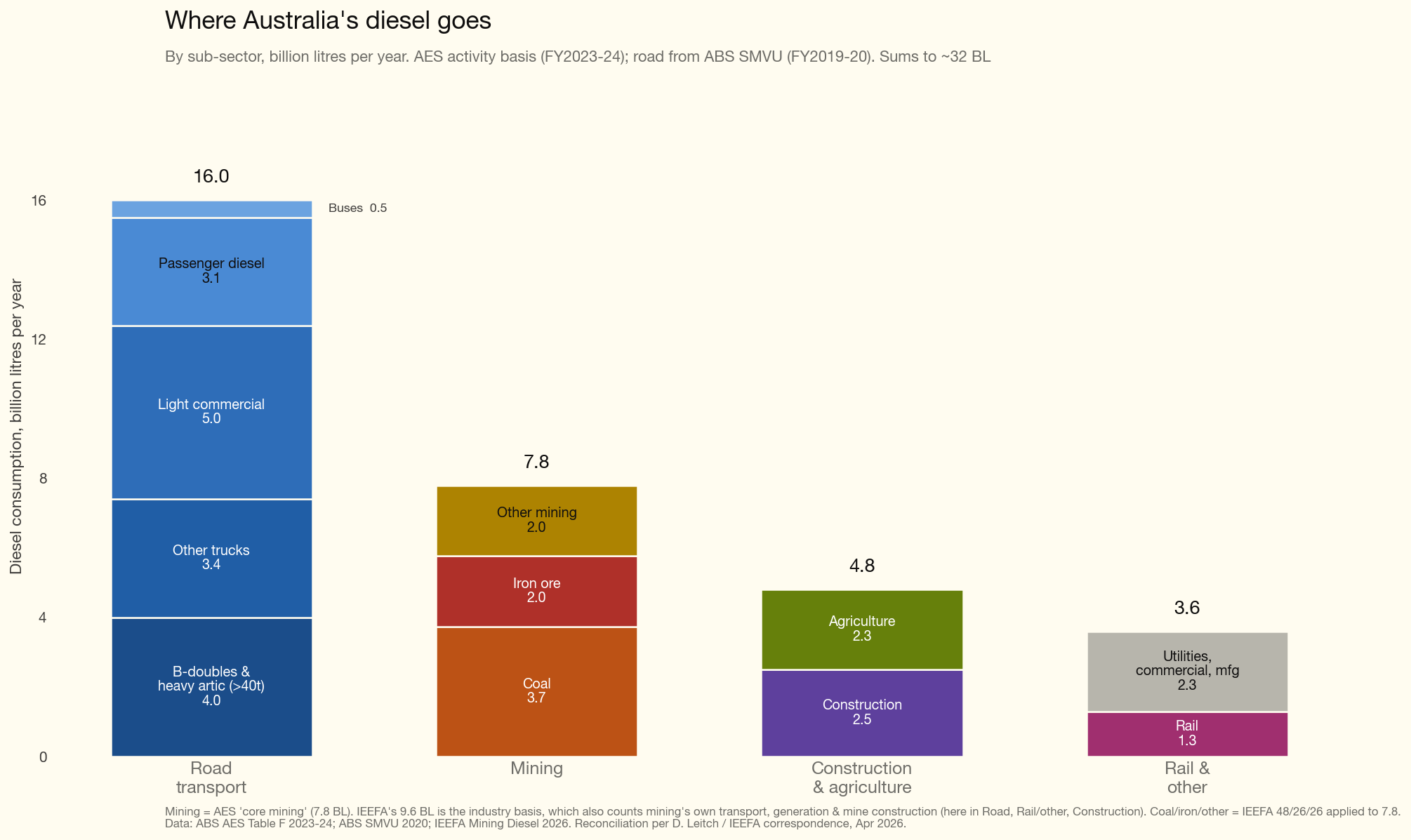

Here’s a reminder of where the diesel goes.

Light commercial is your dual cab utes and vans.

The amount of diesel used in coal mining is a topic in itself. Virtually everyone I know thinks that this is best addressed in the first instance by gradually reducing the diesel fuel rebate over time and using the revenue received in that way to incentivise a switch to electric haul trucks. However, electrifying coal transport is an irony that cuts too close to the bone — even for an investment banker.

So let’s focus on road transport. First let’s look at what the world leader, China, is doing.

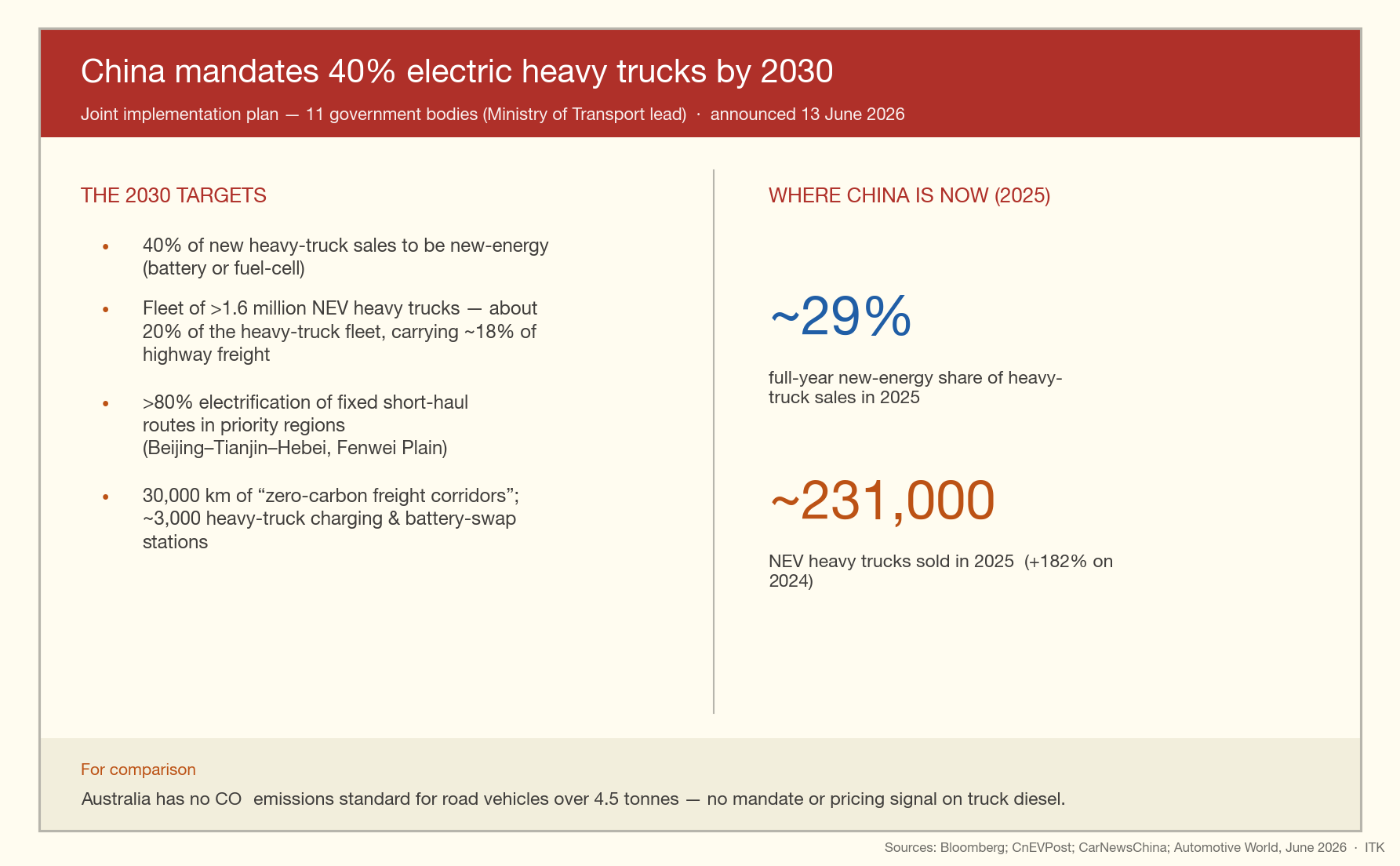

Learn from China - it’s easily the world leader in electric trucks

China is also very active in the mining sector. Here are a couple of photos from the XCMG electric mining equipment factory that the Smart Energy/RECAP/Austrade delegation visited.

XCMG in partnership with BYD makes their battery packs on site. I did not personally visit the electric road truck section of XCMG on this tour — it was either trucks or mining equipment, and the mining equipment makes more spectacular photos. But I was told that the truck division’s annual capacity is 70,000 per year and it’s sold out. Electric mining equipment is 30% (smaller) to 100% (larger equipment) more expensive than diesel right now. I suspect there are many reasons for this, one of which is that the division is still in its infancy and costs will come down. For instance the electric motors are custom designed and much lower volume than an electric car motor.

The mining equipment division is only about 10% electric this year but it will be a lot more over the next couple of years. There are good reasons for this, Chinese domestic residential and commercial construction is in a decade long recession. Mining is not and XCMG also has 50% exports.

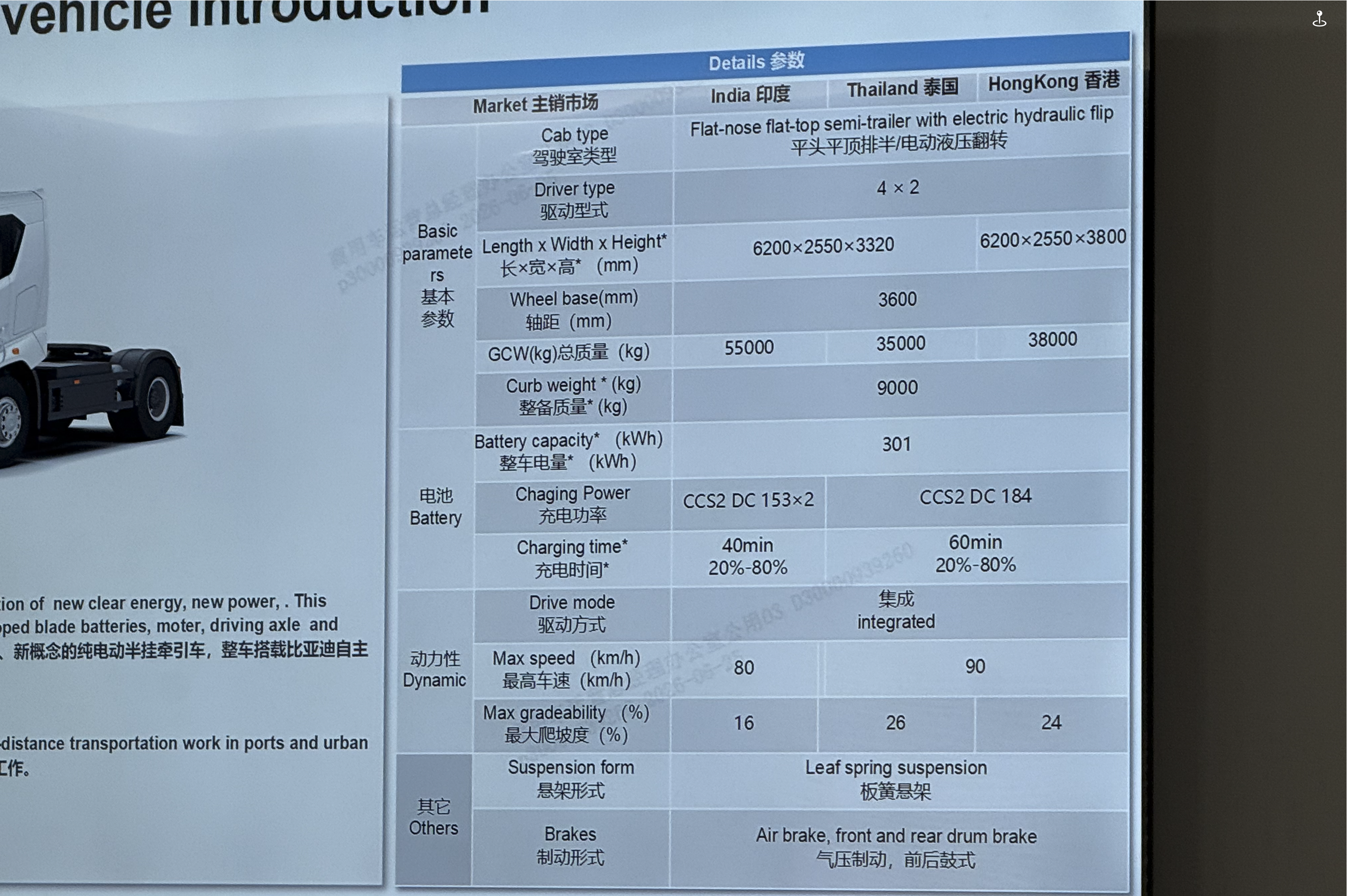

Regarding lighter electric here is a photo from the BYD electric truck factory.

Note the battery on the back of the middle truck in this photo. I did a poor job of photography at BYD. Cabin interiors were very, very basic compared to a modern Chinese electric car.

This would be the place to compliment Austrade and Smartenergy/Recap for organising this tour. Some of the best money I have ever spent on professional development. You might say at my age why am I doing professional development and the answer would be because I just loved it.

If you are a policy developer, investor or business person in this space, run don’t walk to go on the next tour

And it’s also the place to compliment those behind the development of Recap which is extending its trade link program and shared learning (residential solar, home batteries) across South East Asia from Bangladesh to Vietnam. Australia’s reputation in Asia in the renewable energy space, already clearly respected, will only grow.

Back to Australia trucking

Australia has no electric truck policy at all right now. So we have the advantage of a clean slate. China has an excellent electric high speed train system, an excellent set of modern roads and EVs everywhere. It’s far ahead of the USA, even the roads are bitumen sealed whereas those in the USA are often left with a concrete only seal, noisy and less pleasant. The point about China’s infrastructure: it’s all been built in the last 25 years.

What this shows is that where there is national will, much can be achieved quickly. Willpower is what’s needed most.

After will power, in my opinion, we need a simple plan. The plan has a target and then the ways in which the target will be achieved.

Trade associations are the key to policy

I learned a lot on this latest trip but one insight surely was how important trade associations, working together with the public service are in developing policy. Trade associations don’t just represent a source of expertise, they also represent a policy support base. Ultimately that’s the failure of the opposition electricity policy. The industry doesn’t support building more coal, much more gas or nuclear. It’s just politicians trying to force things through without support.

On the other hand the home battery scheme, novated leases have plenty of support from the relevant industries and were developed with input from the relevant trade bodies.

EV trucks don’t really have a strong industry identity yet. It’s a collection of groups that put together the national EV trucking day in Canberra earlier this year. That day was a success but it also showed me that the essential behind the scenes policy development, the departmental briefings, the ministerial awareness were entirely lacking.

I have myself some strong ideas about the appropriate policies. These would include dividing EV trucks by their charging requirements. Within an urban area, chargers suitable for light commercial vehicles are required. Probably not much different to EV chargers except they will be drive through with numerous bays. Time is money for all transport drivers. But 150–250 kW per bay will do this group.

Once we get into vehicles with 250 kWh and up size batteries then we need purpose built charging infrastructure. Arguably this should be mapped out. It may be that existing truck stations on major highways can be part converted.

Finance for truck owners, and changes to taxes, registration, weight limits and standards.

China’s approach to charging and batteries

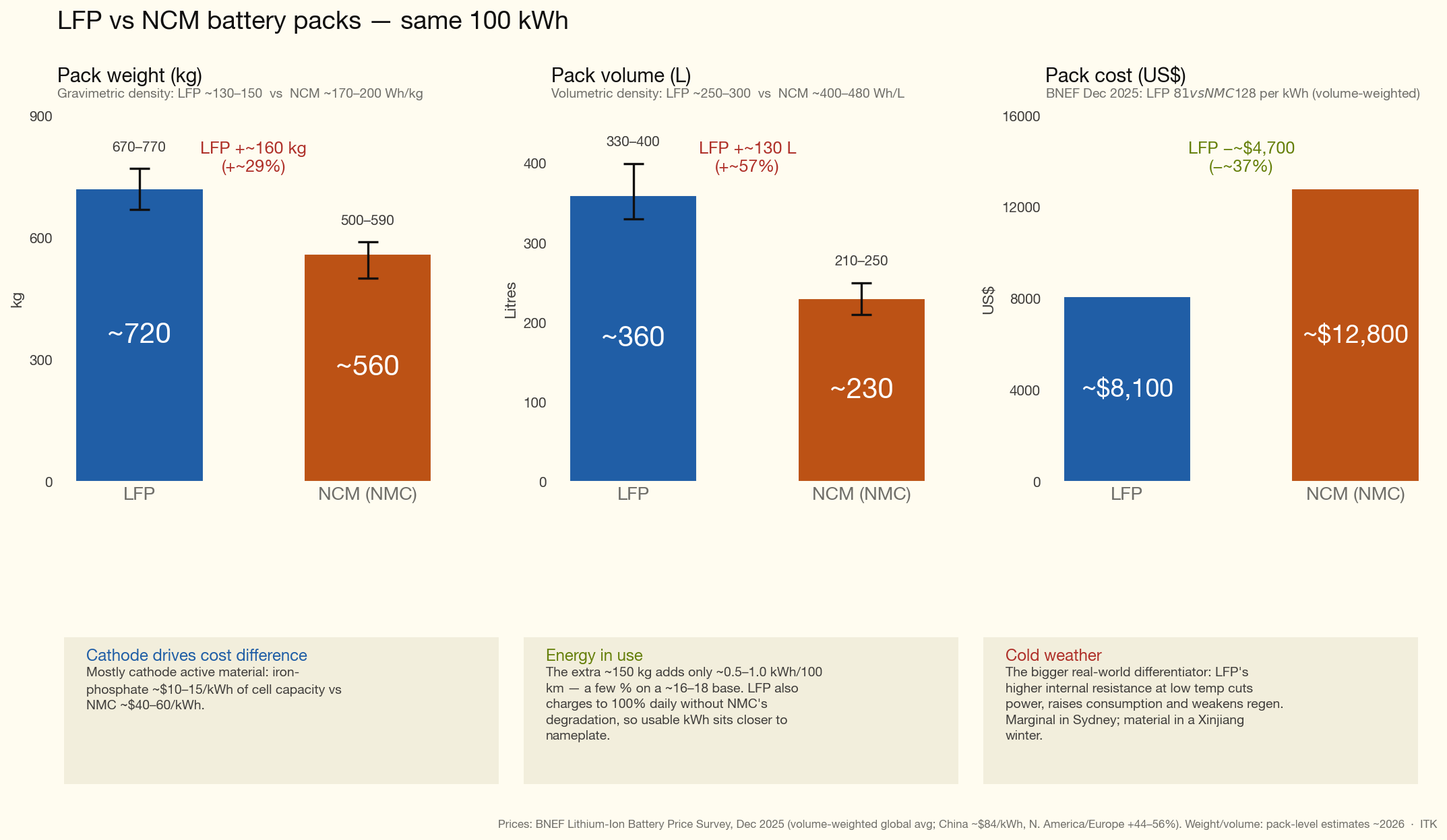

In China the focus is clearly to move from NMC to LFP batteries at all levels of EVs. The reason is basically cost but comes with performance drawbacks. The higher weight requires heavier suspension and so on and impacts vehicle performance.

So China’s strategy to deal with the performance drawbacks is to use smaller packs but have faster charging available.

At the cathode-material level, NMC is actually the better fast-charger.

But the cathode usually isn’t the constraint — the graphite anode is. Fast-charge risk is dominated by lithium plating on the anode (same graphite in both chemistries) and by heat.

- Thermal headroom. LFP’s thermal-runaway onset is ~270 °C vs ~210 °C for NMC, so you can push more current and tolerate more pack heating with a smaller safety penalty.

- Degradation tolerance. LFP shrugs off the cycle-life hit that fast charging inflicts. CATL’s 3rd-gen Shenxing claims retention above 90% after 1,000 ultra-fast charge cycles.

- Electrode engineering. Lower energy density means lower areal loading and thinner electrodes are viable, giving more surface area per kWh to accept current and shed heat.

At CATL’s April 2026 Tech Day, the 3rd-gen Shenxing LFP hit an equivalent 10C and peak 15C rate — 10–80% SoC in 3 min 44 s, 10–98% in 6 min 27 s, achieved via the industry’s lowest internal resistance at 0.25 milliohms, roughly half the typical figure. BYD’s Blade 2.0 does 10–70% in 5 minutes.

NMC’s charging limitation was never fundamental. At that same 2026 event, CATL’s 3rd-gen Qilin NMC matched Shenxing’s charging speed — 10C-equivalent charging, 3,000 kW peak discharge, 1,000 km+ range, and 280 Wh/kg, a product the coverage notes BYD has no equivalent to.

The strategic framing CATL itself gave is the useful one here: LFP is nearing its theoretical energy-density ceiling, so its roadmap is pivoting to extreme fast charging as the differentiator, while NMC keeps energy density as its leadership metric. Fast charging is becoming LFP’s headline selling point precisely because it can’t win on density but its so much cheaper its becoming dominant.

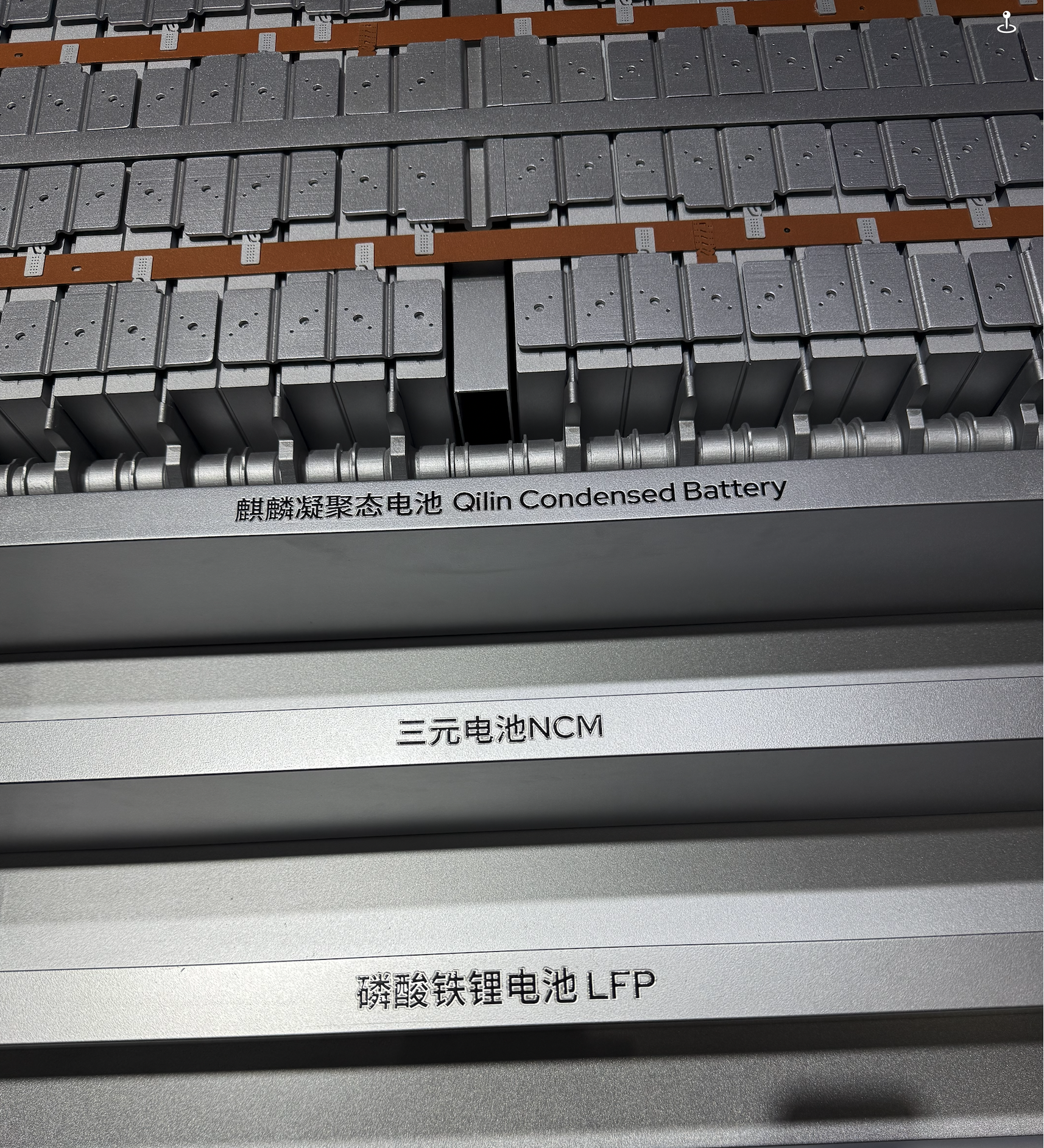

As it happens I spent more time than most delegates looking at the CATL stand at the trade show. This photo shows an extract from a model CATL presented of the volume of the Qilin pack compared to LFP and NMC

Relevance to BYD’s 1 MW flash charger

BYD has taken the fast charging to an extreme with its up to or even over 1 MW flash charger. At the BYD factory, management showed us a flash charger. We delegates had some discussion over whether it really could flash charge. We had that discussion because the cable and the connector to the car were not particularly heavy duty to look at. And so at the risk of boring everyone else and being a pest I insisted on asking a question at the group session about how it worked. Management chatted away and after a couple of minutes I heard the answer.

Part of the answer was the exact opposite to what I would have assumed, so I had to have a long session with Claude to discuss things.

First let’s look at the two photos which show the dispenser and the cabinets. Not very good photos but by now that’s what you come to expect.

One part of the charging answer is that the charger has a battery which acts as a buffer. So input power might be 100 kW but output power can be 1000 kW. Of course eventually the battery will empty but lets not worry.

The other point which is where management really helped me was to explain that the charging cable is hollow. This was what threw me, because everyone knows that the thicker the cable is the more current it can carry.

But Claude couldn’t find any reference to the hollow cable, and the conclusion we reached was that the cable is liquid cooled. The liquid cooling conducts heat away quickly and effectively, enabling the high current to be sustained.

However car packs can’t take more than 10 C

So there is a reasonable explanation of the charger. On the other end, even though modern LFP batteries can take 10C, that means you need a 100 kWh pack to take a 1 MW charge. And personally I would worry about a 10C charge rate. In my model plane batteries I rarely go over 3C.

Real world data bears this out. The Han L carries an 83.2 kWh pack. A real-world Han L session started at 464 kW, hit the 1,000 kW peak around the 18-second mark, sustained that peak for roughly 40 seconds, then dropped to 660 kW; 5–50% took 3 min 33 s before the rate fell to ~467 kW. So the megawatt is a ~40-second spike at low SoC, not a plateau. Average it out and one analysis estimated the average C-rate over the 10–62% window was about 5–6C. Average charge rate 550 kW.

Ha ha — not that any charger in Australia can do 550 kW. Half of them struggle to do 50 kW.

Nevertheless China has shown that the way forward is LFP batteries and fast chargers. That’s the message for Australia.

Diesel is where the trade balance, the jobs and the strategic exposure all sit, and solar charged batteries are the way to replace it. China has done the hard work of proving the technology and the charging model. Our job is easier: a clean slate, a simple plan with a target, the trade associations and the public service working together, and the willpower to start. The winners get the prizes. We should be racing to be one of them.